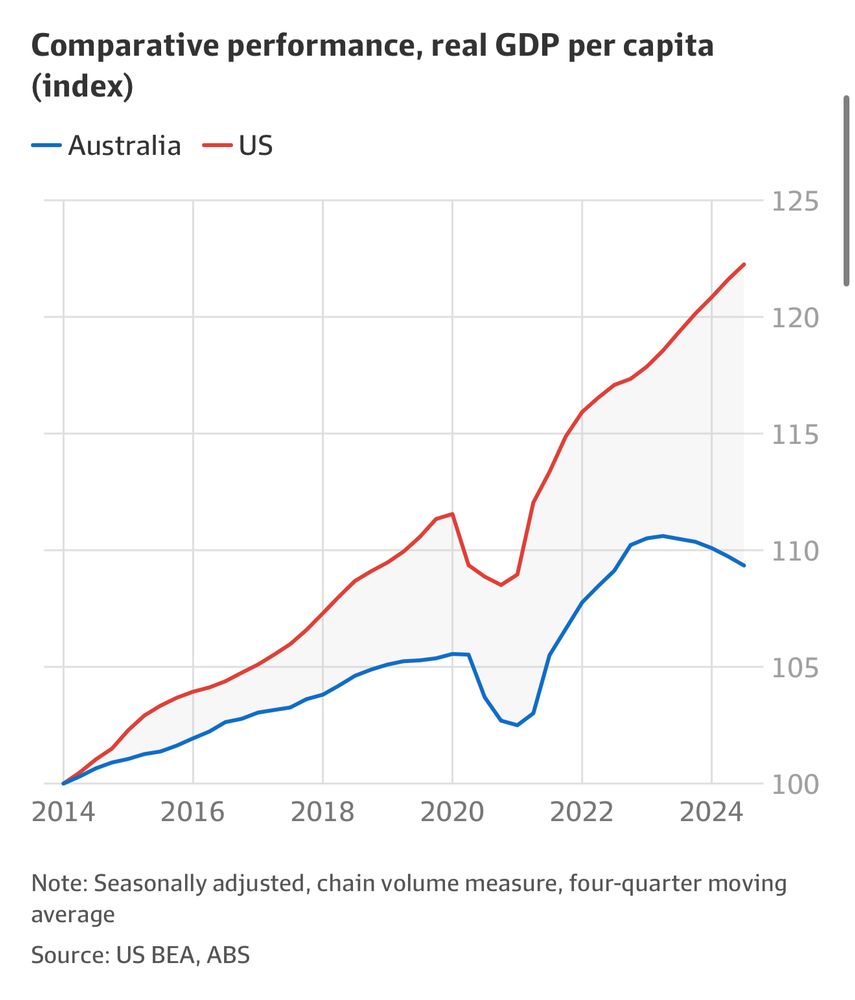

As you can see in my chart in the piece, I am referring to per-capita GDP, a commonly used indicator of living standards. The two countries’ statistical agencies are the source as noted in the chart note.

February 2, 2025 at 5:02 PM

As you can see in my chart in the piece, I am referring to per-capita GDP, a commonly used indicator of living standards. The two countries’ statistical agencies are the source as noted in the chart note.

The audience for this thread was people who might referee my paper.

December 17, 2024 at 10:43 PM

The audience for this thread was people who might referee my paper.

Yes, that would be included in the complement of our spending measure. You are not typical!

December 17, 2024 at 10:39 PM

Yes, that would be included in the complement of our spending measure. You are not typical!

However, it's nice that the broad swathe of the calibration results is consistent with previous versions of our paper.

Thanks for getting this far! Please read the paper, circulate to those who might be interested, and let us know what you think.

/Fin

Thanks for getting this far! Please read the paper, circulate to those who might be interested, and let us know what you think.

/Fin

December 17, 2024 at 5:20 PM

However, it's nice that the broad swathe of the calibration results is consistent with previous versions of our paper.

Thanks for getting this far! Please read the paper, circulate to those who might be interested, and let us know what you think.

/Fin

Thanks for getting this far! Please read the paper, circulate to those who might be interested, and let us know what you think.

/Fin

We think this more comprehensive modeling exercise does a better job of reflecting the practical features of the program we study (now including retirement and endogenous withdrawal). And incorporating preference heterogeneity allows us to better match the data and recent work.

December 17, 2024 at 5:20 PM

We think this more comprehensive modeling exercise does a better job of reflecting the practical features of the program we study (now including retirement and endogenous withdrawal). And incorporating preference heterogeneity allows us to better match the data and recent work.

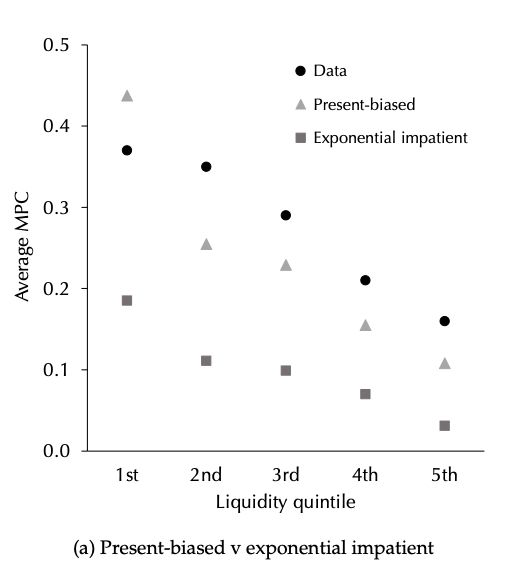

These results make sense. Withdrawal is easy to reconcile but the size and sharpness of the (mostly non-durable) spending response is not. Liquidity constraints are necessary but not sufficient. Present bias by nature reconciles discordant stocks (liquidity) and flows (spending).

December 17, 2024 at 5:20 PM

These results make sense. Withdrawal is easy to reconcile but the size and sharpness of the (mostly non-durable) spending response is not. Liquidity constraints are necessary but not sufficient. Present bias by nature reconciles discordant stocks (liquidity) and flows (spending).

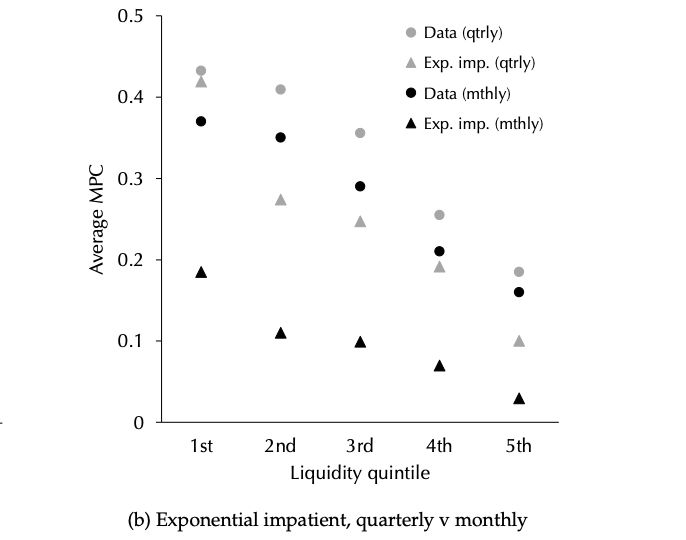

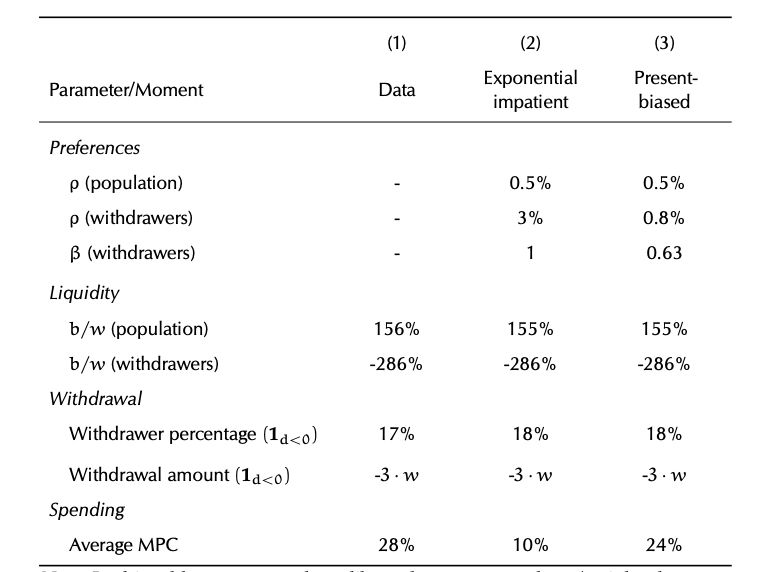

Our fourth main calibration result: the calibration frequency is critical. We use weekly transaction data to observe a sharp spending response (90% within 4 weeks), so we calibrate at a monthly frequency. At a quarterly frequency, the exponential version almost matches the data.

December 17, 2024 at 5:20 PM

Our fourth main calibration result: the calibration frequency is critical. We use weekly transaction data to observe a sharp spending response (90% within 4 weeks), so we calibrate at a monthly frequency. At a quarterly frequency, the exponential version almost matches the data.

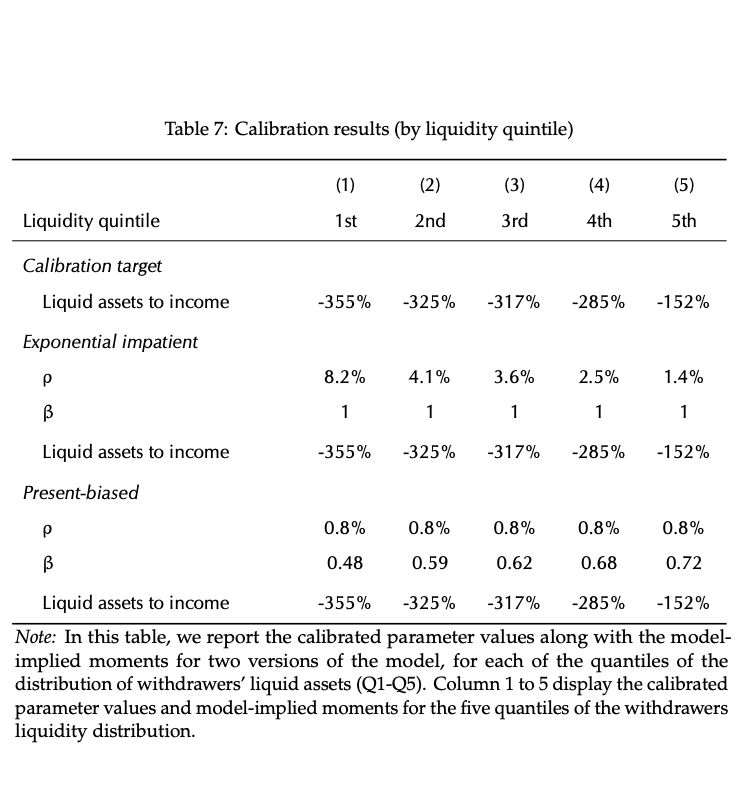

Our third main calibration result: the present-bias version of the model does a much better job of matching the joint distribution of liquidity and spending responses, with parameter values across the whole distribution that are in the ballpark of those in the recent literature.

December 17, 2024 at 5:20 PM

Our third main calibration result: the present-bias version of the model does a much better job of matching the joint distribution of liquidity and spending responses, with parameter values across the whole distribution that are in the ballpark of those in the recent literature.

Our second main calibration result: however, only the present-bias version of the model is able to simultaneously match the pre-withdrawal liquidity distribution and the size and speed of the observed spending response. Note the difference in predicted MPCs in the bottom row.

December 17, 2024 at 5:20 PM

Our second main calibration result: however, only the present-bias version of the model is able to simultaneously match the pre-withdrawal liquidity distribution and the size and speed of the observed spending response. Note the difference in predicted MPCs in the bottom row.

Our first main calibration result: both heterogeneous impatience and heterogeneous present bias can predict the withdrawal patterns we observe given average parameter values (discount factors and present-bias parameters) that are in the ballpark of those in the recent literature.

December 17, 2024 at 5:20 PM

Our first main calibration result: both heterogeneous impatience and heterogeneous present bias can predict the withdrawal patterns we observe given average parameter values (discount factors and present-bias parameters) that are in the ballpark of those in the recent literature.

We model the policy as a temporary reduction in the (arbitrarily high) cost of withdrawing from the retirement account.

We compare two types of preferences in the model: heterogeneous exponential discounting (impatience) and heterogeneous hyperbolic discounting (present bias).

We compare two types of preferences in the model: heterogeneous exponential discounting (impatience) and heterogeneous hyperbolic discounting (present bias).

December 17, 2024 at 5:20 PM

We model the policy as a temporary reduction in the (arbitrarily high) cost of withdrawing from the retirement account.

We compare two types of preferences in the model: heterogeneous exponential discounting (impatience) and heterogeneous hyperbolic discounting (present bias).

We compare two types of preferences in the model: heterogeneous exponential discounting (impatience) and heterogeneous hyperbolic discounting (present bias).

To do so, we develop a heterogeneous-agent model incorporating retirement, two assets, idiosyncratic income risk, borrowing constraints, and preference heterogeneity, and use it to study the effects of the early superannuation withdrawal program on both withdrawal and spending.

December 17, 2024 at 5:20 PM

To do so, we develop a heterogeneous-agent model incorporating retirement, two assets, idiosyncratic income risk, borrowing constraints, and preference heterogeneity, and use it to study the effects of the early superannuation withdrawal program on both withdrawal and spending.

On the face of it, there may be many reasons to observe these withdrawal and spending patterns. For this new version, we overhauled our calibration exercise, in which we seek formally to discern the roles of liquidity constraints and preferences in driving the observed responses.

December 17, 2024 at 5:20 PM

On the face of it, there may be many reasons to observe these withdrawal and spending patterns. For this new version, we overhauled our calibration exercise, in which we seek formally to discern the roles of liquidity constraints and preferences in driving the observed responses.

The empirical results are unchanged since the first version from March 2023. The key results are:

1) strong selection into withdrawing retirement savings on the basis of poor financial health; and

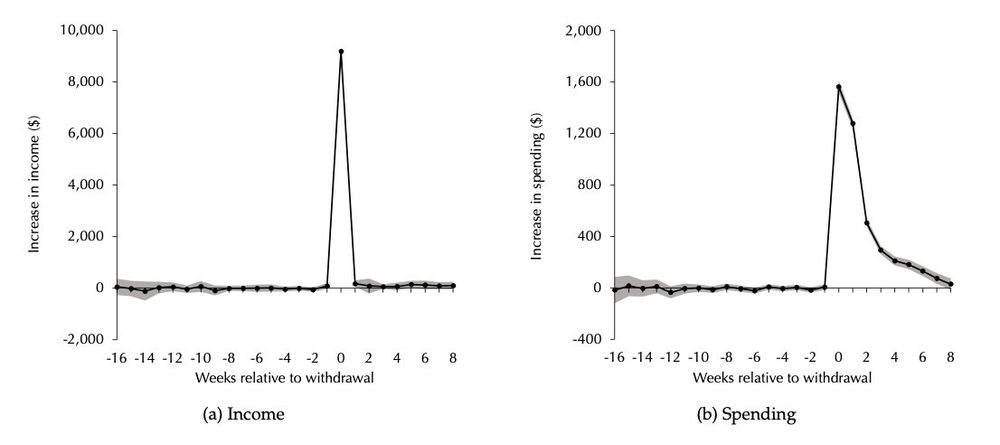

2) a very large and sharp spending response, positively correlated with selection.

1) strong selection into withdrawing retirement savings on the basis of poor financial health; and

2) a very large and sharp spending response, positively correlated with selection.

December 17, 2024 at 5:20 PM

The empirical results are unchanged since the first version from March 2023. The key results are:

1) strong selection into withdrawing retirement savings on the basis of poor financial health; and

2) a very large and sharp spending response, positively correlated with selection.

1) strong selection into withdrawing retirement savings on the basis of poor financial health; and

2) a very large and sharp spending response, positively correlated with selection.

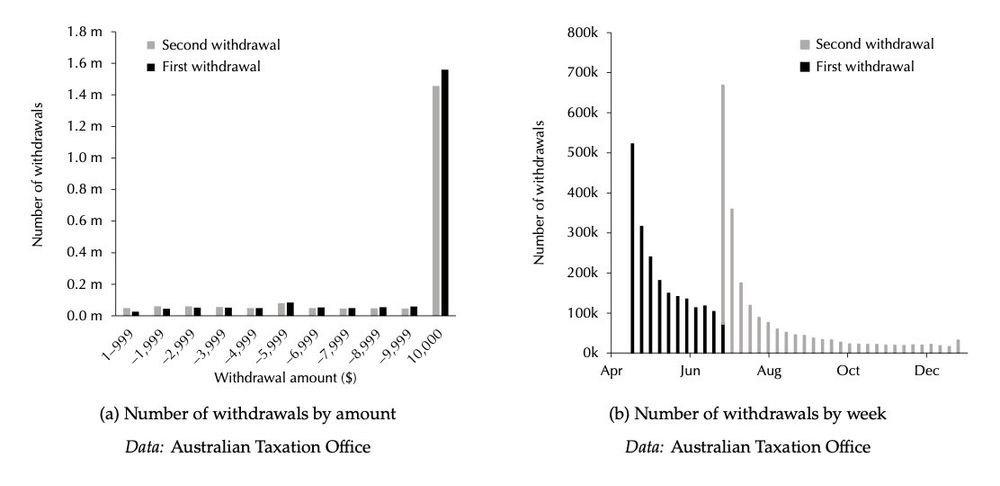

During the pandemic, Australia for the first time allowed people to withdraw up to $20k from their normally illiquid mandatory private retirement saving accounts. 1 in 6 people withdrew a total of 2% of GDP. We use admin and bank transaction data to study withdrawal and spending.

December 17, 2024 at 5:20 PM

During the pandemic, Australia for the first time allowed people to withdraw up to $20k from their normally illiquid mandatory private retirement saving accounts. 1 in 6 people withdrew a total of 2% of GDP. We use admin and bank transaction data to study withdrawal and spending.

More from me on this in tomorrow’s Financial Review.

December 15, 2024 at 4:10 AM

More from me on this in tomorrow’s Financial Review.

Rather than the 44% nuclear cost saving claimed by the coalition, the true nuclear cost saving claimed by the modelling is actually just 12%. But because the modelling uses an implausibly low capital cost and high capacity factor for nuclear, even this 12% claim isn't credible.

December 15, 2024 at 4:10 AM

Rather than the 44% nuclear cost saving claimed by the coalition, the true nuclear cost saving claimed by the modelling is actually just 12%. But because the modelling uses an implausibly low capital cost and high capacity factor for nuclear, even this 12% claim isn't credible.

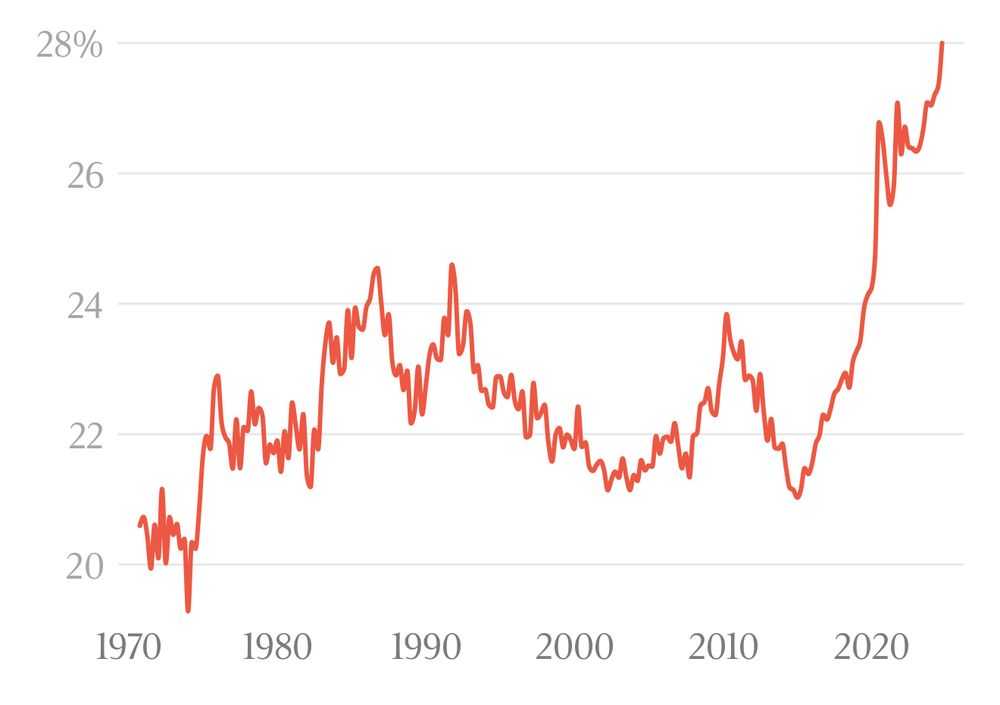

Yes. Government spending as a percentage of GDP has risen from 24.5% of GDP, around its historic average, to more than 27% of GDP in just two years. The public sector is exploding.

December 9, 2024 at 5:57 PM

Yes. Government spending as a percentage of GDP has risen from 24.5% of GDP, around its historic average, to more than 27% of GDP in just two years. The public sector is exploding.