Isabel Schnabel 🇪🇺🇺🇦

@isabelschnabel.bsky.social

Executive Board of the European Central Bank, University of Bonn (on leave) #NieWiederIstJetzt

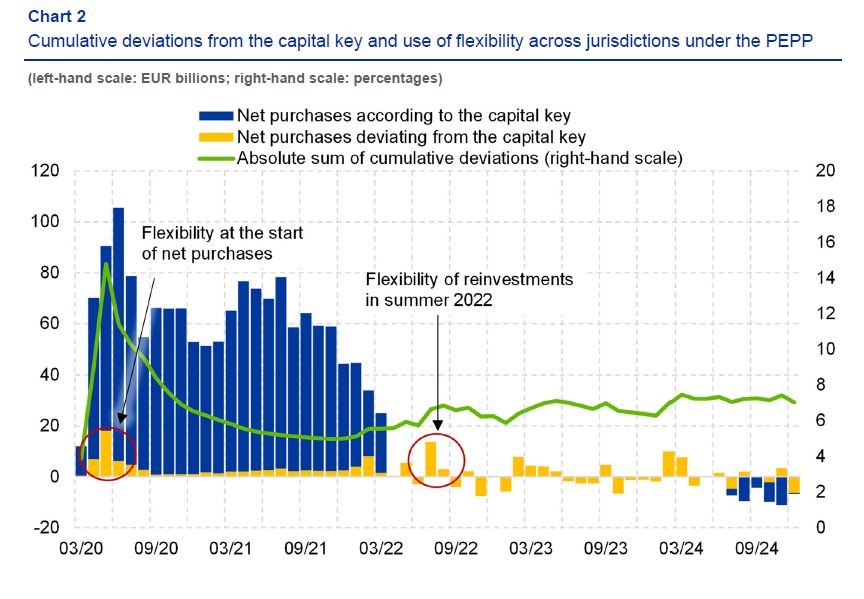

As regards the use of flexibility, the vast majority of purchases were conducted in line with the capital key. Besides technical factors, deviations occurred at the start of the PEPP in 2020 and in the summer of 2022, responding to risks to the transmission of monetary policy (red circles). 4/6

May 2, 2025 at 8:40 AM

As regards the use of flexibility, the vast majority of purchases were conducted in line with the capital key. Besides technical factors, deviations occurred at the start of the PEPP in 2020 and in the summer of 2022, responding to risks to the transmission of monetary policy (red circles). 4/6

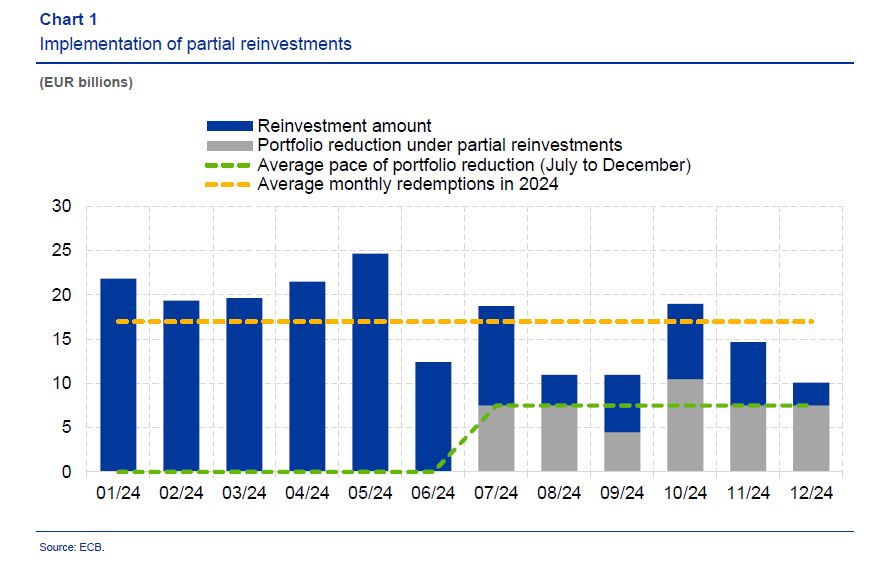

The new data give more insights into the implementation during the reinvestment phase. It shows how the Eurosystem balanced its market presence, taking seasonal patterns of redemptions and issuance into account. 3/6

May 2, 2025 at 8:40 AM

The new data give more insights into the implementation during the reinvestment phase. It shows how the Eurosystem balanced its market presence, taking seasonal patterns of redemptions and issuance into account. 3/6

P.S.: As always, the full speech and slides are on the ECB's website.

A special thanks to @andrespicer.bsky.social, @vassoioannidou.bsky.social and Bayes Business School as whole for welcoming me so warmly!

A special thanks to @andrespicer.bsky.social, @vassoioannidou.bsky.social and Bayes Business School as whole for welcoming me so warmly!

March 30, 2025 at 3:42 PM

P.S.: As always, the full speech and slides are on the ECB's website.

A special thanks to @andrespicer.bsky.social, @vassoioannidou.bsky.social and Bayes Business School as whole for welcoming me so warmly!

A special thanks to @andrespicer.bsky.social, @vassoioannidou.bsky.social and Bayes Business School as whole for welcoming me so warmly!

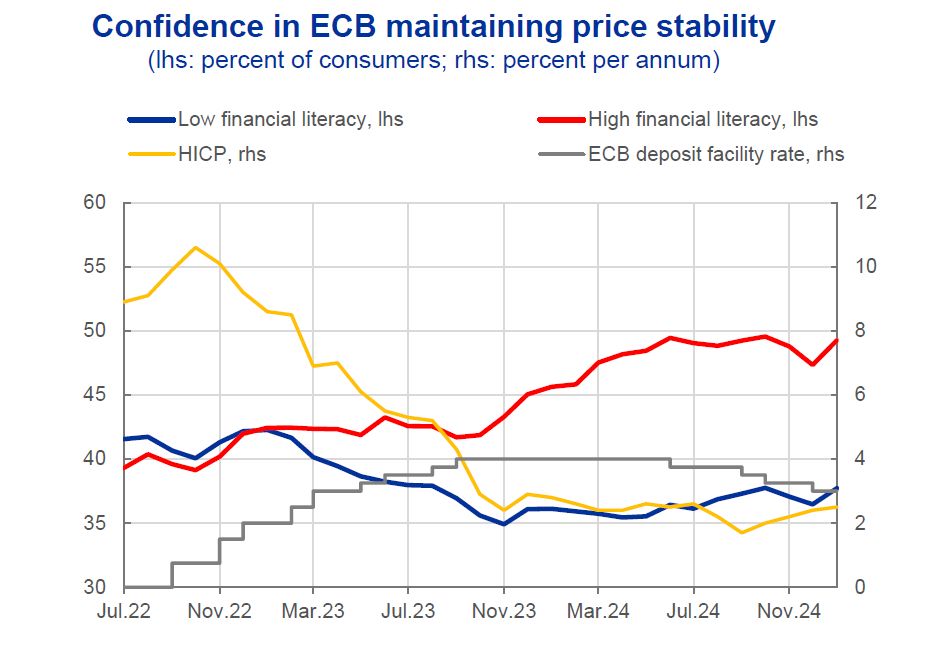

In the most recent inflationary episode, the share of households with high financial literacy that trusted the ECB to maintain price stability rose notably as interest rates rose and inflation came down, while less financially literate households lost confidence. 18/22

March 30, 2025 at 3:42 PM

In the most recent inflationary episode, the share of households with high financial literacy that trusted the ECB to maintain price stability rose notably as interest rates rose and inflation came down, while less financially literate households lost confidence. 18/22

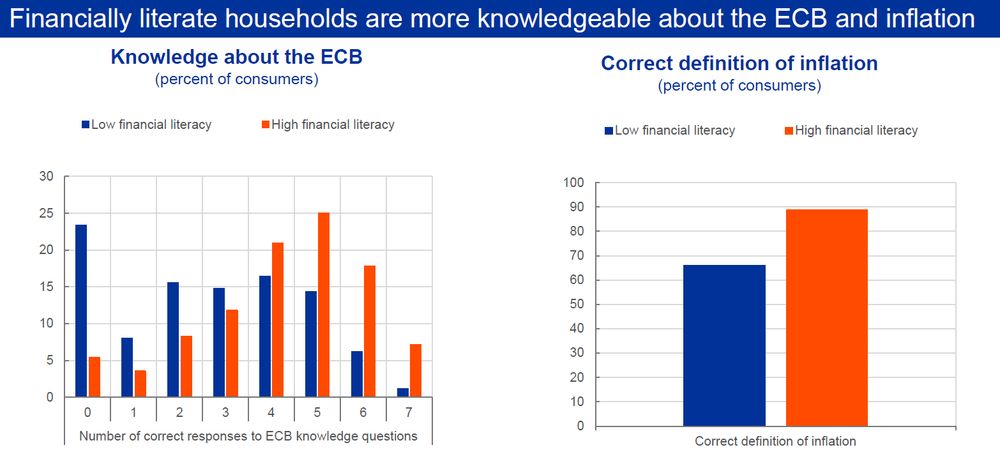

When people better understand monetary policy, they trust central banks more, which helps anchor inflation expectations. Financially literate households are more knowledgeable about the ECB and more likely to know the correct definition of inflation, affecting the ECB’s credibility. 17/22

March 30, 2025 at 3:42 PM

When people better understand monetary policy, they trust central banks more, which helps anchor inflation expectations. Financially literate households are more knowledgeable about the ECB and more likely to know the correct definition of inflation, affecting the ECB’s credibility. 17/22

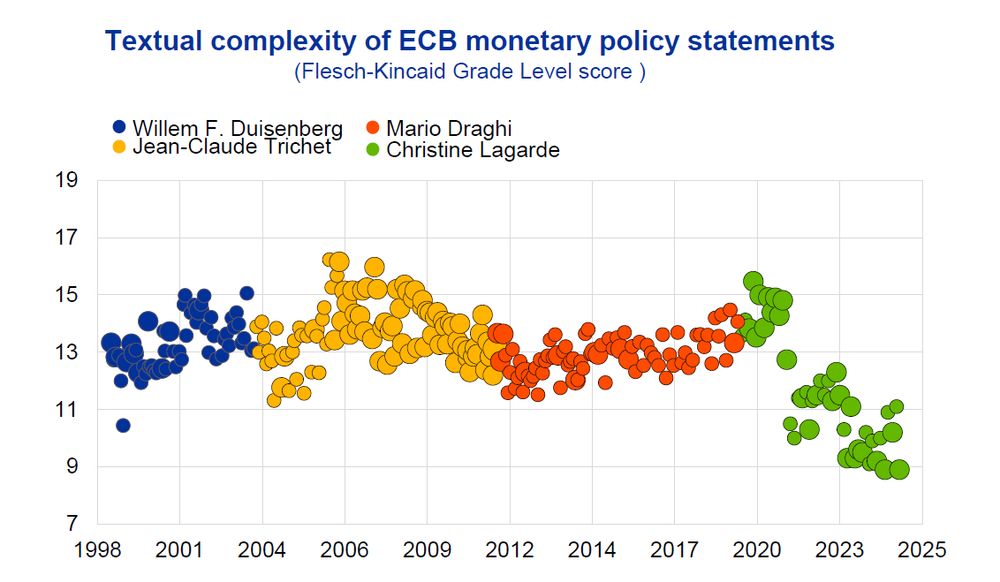

Since our 2021 monetary policy strategy review, we have put more emphasis on explaining our monetary policy decisions to the general public in an accessible way. Our new monetary policy statement is less complex, which increases its readability. 15/22

March 30, 2025 at 3:42 PM

Since our 2021 monetary policy strategy review, we have put more emphasis on explaining our monetary policy decisions to the general public in an accessible way. Our new monetary policy statement is less complex, which increases its readability. 15/22

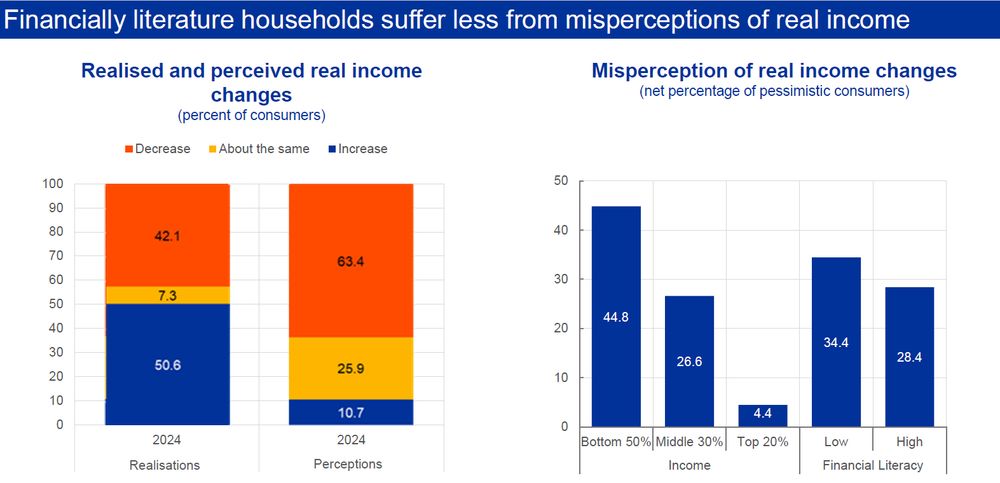

Financial literacy also affects household perceptions of real income. While 50% of households experienced positive real income growth in 2024, only 11% perceived that their real income had increased. The degree of misperception depends negatively on income and financial literacy. 14/22

March 30, 2025 at 3:42 PM

Financial literacy also affects household perceptions of real income. While 50% of households experienced positive real income growth in 2024, only 11% perceived that their real income had increased. The degree of misperception depends negatively on income and financial literacy. 14/22

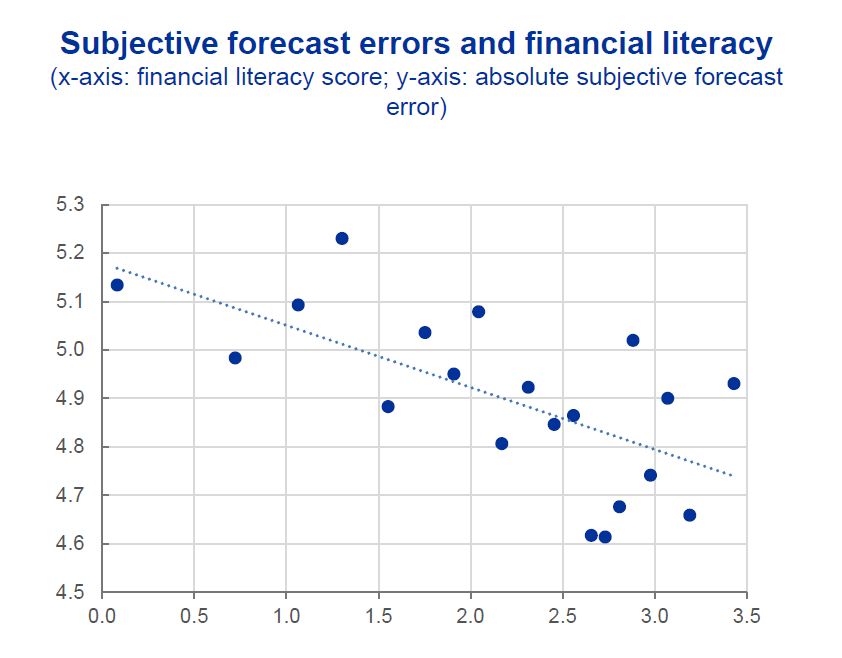

The observed differences in the formation of inflation expectations translate into lower subjective forecast errors for more financially literate people. Hence, households with higher levels of financial literacy tend to have more accurate inflation expectations. 13/22

March 30, 2025 at 3:42 PM

The observed differences in the formation of inflation expectations translate into lower subjective forecast errors for more financially literate people. Hence, households with higher levels of financial literacy tend to have more accurate inflation expectations. 13/22

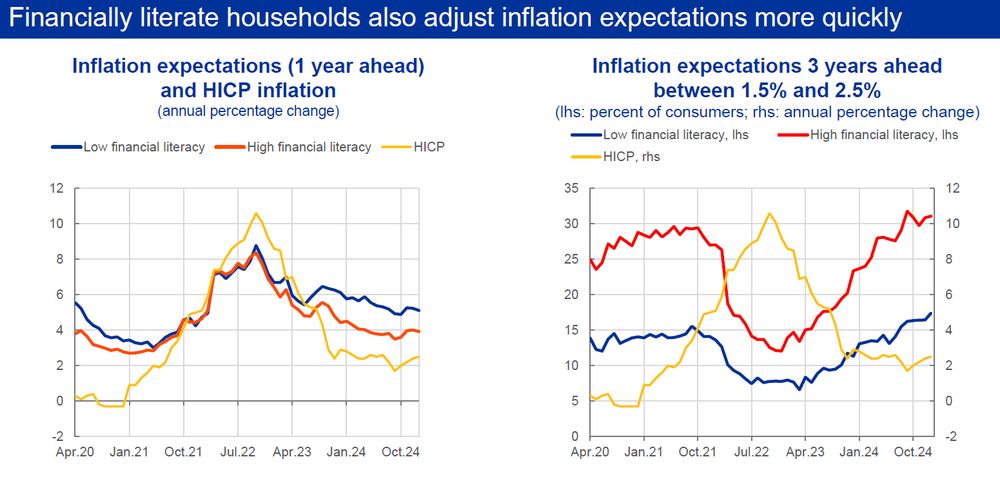

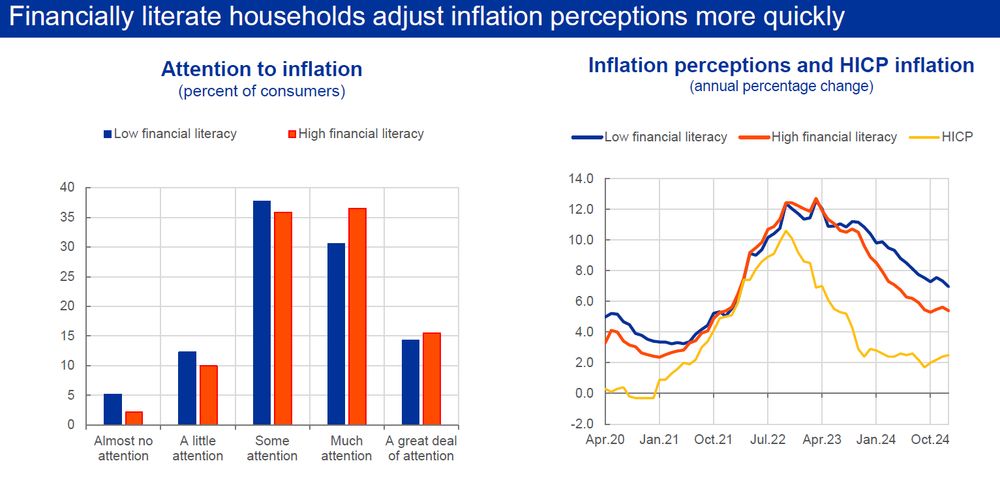

Similarly, inflation expectations of financially literate households have dropped more quickly. While the share of consumers with inflation expectations broadly anchored around 2% has been low overall, the financially literate are more responsive to actual inflation developments. 12/22

March 30, 2025 at 3:42 PM

Similarly, inflation expectations of financially literate households have dropped more quickly. While the share of consumers with inflation expectations broadly anchored around 2% has been low overall, the financially literate are more responsive to actual inflation developments. 12/22

Survey evidence indicates that households with higher financial literacy pay more attention to inflation. However, even for financially literate people, inflation perceptions of past inflation are often very persistent, adapting slowly to actual inflation dynamics. 11/22

March 30, 2025 at 3:42 PM

Survey evidence indicates that households with higher financial literacy pay more attention to inflation. However, even for financially literate people, inflation perceptions of past inflation are often very persistent, adapting slowly to actual inflation dynamics. 11/22

Second, financially literate people are more willing to take on risk. They are much more likely to invest in stocks or mutual funds, and are slightly more likely to take out mortgages. This may strengthen monetary policy transmission. But there are also effects going in the opposite direction. 9/22

March 30, 2025 at 3:42 PM

Second, financially literate people are more willing to take on risk. They are much more likely to invest in stocks or mutual funds, and are slightly more likely to take out mortgages. This may strengthen monetary policy transmission. But there are also effects going in the opposite direction. 9/22

Financial literacy of customers also affects how swiftly and strongly banks pass through changes in policy rates. Financially literate households are more likely to “shop around” for the best terms of debt products. Corporates received higher deposits rates than households. 8/22

March 30, 2025 at 3:42 PM

Financial literacy of customers also affects how swiftly and strongly banks pass through changes in policy rates. Financially literate households are more likely to “shop around” for the best terms of debt products. Corporates received higher deposits rates than households. 8/22

Moreover, financially literate households preferred fixed-rate loans when interest rates were low but less so when interest rates were high. Longer fixation periods slow down policy transmission. Again, financially less literate households reacted much less to the interest rate environment. 7/22

March 30, 2025 at 3:42 PM

Moreover, financially literate households preferred fixed-rate loans when interest rates were low but less so when interest rates were high. Longer fixation periods slow down policy transmission. Again, financially less literate households reacted much less to the interest rate environment. 7/22

When the @ecb.europa.eu raised its policy rates in 2022 to fight inflation, financially literate individuals understood that this created more beneficial conditions for saving and less attractive conditions for borrowing. By contrast, less financially literate people reacted much less. 6/22

March 30, 2025 at 3:42 PM

When the @ecb.europa.eu raised its policy rates in 2022 to fight inflation, financially literate individuals understood that this created more beneficial conditions for saving and less attractive conditions for borrowing. By contrast, less financially literate people reacted much less. 6/22

First, financially literate households are more responsive to changes in interest rates. One reason is that these households (shown in red) are more attentive to interest rate developments than the less financially literate (shown in blue). 5/22

March 30, 2025 at 3:42 PM

First, financially literate households are more responsive to changes in interest rates. One reason is that these households (shown in red) are more attentive to interest rate developments than the less financially literate (shown in blue). 5/22

In the euro area, only 48% can answer the “Big Three” questions on financial literacy, asking about compound interest, inflation and risk diversification. Financial literacy is lower for younger people, women, the less educated and people with lower incomes. 3/22

March 30, 2025 at 3:42 PM

In the euro area, only 48% can answer the “Big Three” questions on financial literacy, asking about compound interest, inflation and risk diversification. Financial literacy is lower for younger people, women, the less educated and people with lower incomes. 3/22

Today I had another exchange with German-speaking economists on the challenges facing the German and euro area economy and what this implies for monetary policy @ecb.europa.eu. One focus was how to make sure that the German packages for defence and infrastructure will become a success. 1/3

March 17, 2025 at 9:55 PM

Today I had another exchange with German-speaking economists on the challenges facing the German and euro area economy and what this implies for monetary policy @ecb.europa.eu. One focus was how to make sure that the German packages for defence and infrastructure will become a success. 1/3

I discuss how the transition to less ample reserves can be facilitated in the future: first, through regular testing to foster operational readiness; second, through pre-positioning of collateral; and third, through central clearing, which could reduce dealer balance sheet constraints. 16/16

February 26, 2025 at 9:38 AM

I discuss how the transition to less ample reserves can be facilitated in the future: first, through regular testing to foster operational readiness; second, through pre-positioning of collateral; and third, through central clearing, which could reduce dealer balance sheet constraints. 16/16

There are three implications for monetary policy. First, a higher r* implies that central banks must proceed cautiously when monetary policy ceases to be restrictive. In the euro area, the bank lending survey suggests that monetary policy may no longer be restrictive. 12/16

February 26, 2025 at 9:38 AM

There are three implications for monetary policy. First, a higher r* implies that central banks must proceed cautiously when monetary policy ceases to be restrictive. In the euro area, the bank lending survey suggests that monetary policy may no longer be restrictive. 12/16

Moreover, geopolitical fragmentation contributes to declining demand for government bonds, as exemplified by the marked decline in the share of foreign official holdings of US Treasury securities. The normalisation of central bank balance sheets is the third important driver. 11/16

February 26, 2025 at 9:38 AM

Moreover, geopolitical fragmentation contributes to declining demand for government bonds, as exemplified by the marked decline in the share of foreign official holdings of US Treasury securities. The normalisation of central bank balance sheets is the third important driver. 11/16

As the net supply of government bonds has increased, as illustrated by the rise in the sovereign bond free float as a share of the outstanding volume, the global savings glut has turned into a global bond glut. One reason is the high level of net borrowing by governments. 10/16

February 26, 2025 at 9:38 AM

As the net supply of government bonds has increased, as illustrated by the rise in the sovereign bond free float as a share of the outstanding volume, the global savings glut has turned into a global bond glut. One reason is the high level of net borrowing by governments. 10/16

Asset swap spreads, a common proxy of the convenience yield, shifted down with QE and fiscal consolidation, because the net supply of government bonds in the market went down. But since mid-2022 they have narrowed and turned positive recently. 9/16

February 26, 2025 at 9:38 AM

Asset swap spreads, a common proxy of the convenience yield, shifted down with QE and fiscal consolidation, because the net supply of government bonds in the market went down. But since mid-2022 they have narrowed and turned positive recently. 9/16

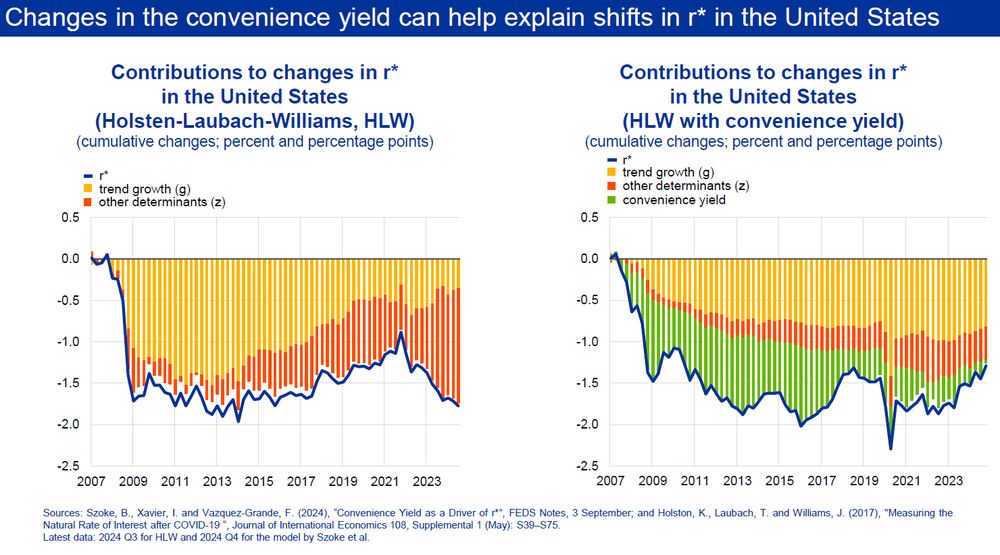

Research by Fed economists shows that incorporating the convenience yield – the yield that investors are willing to forgo in equilibrium for liquidity and safety services of government bonds – into the Laubach-Williams model significantly improves the explanatory power of the model. 7/16

February 26, 2025 at 9:38 AM

Research by Fed economists shows that incorporating the convenience yield – the yield that investors are willing to forgo in equilibrium for liquidity and safety services of government bonds – into the Laubach-Williams model significantly improves the explanatory power of the model. 7/16

The same dynamics are reflected in model-based estimates of r*. According to an analysis by ECB economists, r* in the euro area has increased even more than forward rates. While it is difficult to pin down the level of r*, the directional change is unambiguously upwards. 4/16

February 26, 2025 at 9:38 AM

The same dynamics are reflected in model-based estimates of r*. According to an analysis by ECB economists, r* in the euro area has increased even more than forward rates. While it is difficult to pin down the level of r*, the directional change is unambiguously upwards. 4/16

Euro area real long-term rates are substantially higher today than during most of the post-2008 period. This is not just driven by the tightening of monetary policy but also by higher real forward rates – a common proxy of the natural rate of interest, r*. 3/16

February 26, 2025 at 9:38 AM

Euro area real long-term rates are substantially higher today than during most of the post-2008 period. This is not just driven by the tightening of monetary policy but also by higher real forward rates – a common proxy of the natural rate of interest, r*. 3/16