Ben Casselman

@bencasselman.bsky.social

Chief Economics Correspondent for The New York Times. Adjunct at CUNY Newmark. Ex: FiveThirtyEight, WSJ. He/him.

Email: [email protected]

Signal: @bencasselman.96

📸: Earl Wilson/NYT

Email: [email protected]

Signal: @bencasselman.96

📸: Earl Wilson/NYT

I'm honored to be delivering the annual Ellen C. Gstalder Memorial Lecture at Georgetown next week. I'm talking about what A.I. will mean for the job market. And since the real answer is "I have no idea," I'll be looking at it through a historical lens.

Details: events.georgetown.edu/event/35638-...

Details: events.georgetown.edu/event/35638-...

November 7, 2025 at 2:42 PM

I'm honored to be delivering the annual Ellen C. Gstalder Memorial Lecture at Georgetown next week. I'm talking about what A.I. will mean for the job market. And since the real answer is "I have no idea," I'll be looking at it through a historical lens.

Details: events.georgetown.edu/event/35638-...

Details: events.georgetown.edu/event/35638-...

Unemployment filings among federal workers fell for a second straight week, but are still very elevated. About 37,000 federal employees have filed for benefits since the shutdown began.

November 7, 2025 at 2:36 PM

Unemployment filings among federal workers fell for a second straight week, but are still very elevated. About 37,000 federal employees have filed for benefits since the shutdown began.

Continuing claims continue to drift up. No surge here either, but definitely consistent with the idea that unemployment is gradually rising, and that it's getting harder to find a job.

November 7, 2025 at 2:36 PM

Continuing claims continue to drift up. No surge here either, but definitely consistent with the idea that unemployment is gradually rising, and that it's getting harder to find a job.

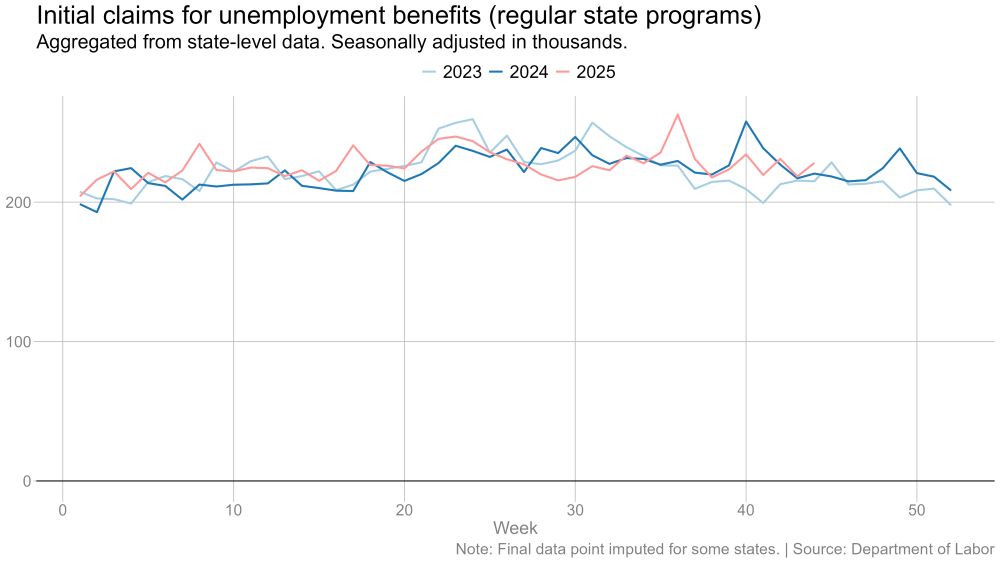

We did get *some* data today: Jobless claims increased slightly in the final week of October. But the four-week average actually fell. Still no sign of a surge in layoffs in these numbers. #NumbersDay

November 7, 2025 at 2:36 PM

We did get *some* data today: Jobless claims increased slightly in the final week of October. But the four-week average actually fell. Still no sign of a surge in layoffs in these numbers. #NumbersDay

Second, this is a very hard labor market to interpret right now. We have good private-sector measures of labor *demand.* But a lot of the action right now is on labor *supply* as a result of big shifts in immigration flows. And we have much less good data on that.

November 7, 2025 at 1:34 PM

Second, this is a very hard labor market to interpret right now. We have good private-sector measures of labor *demand.* But a lot of the action right now is on labor *supply* as a result of big shifts in immigration flows. And we have much less good data on that.

So far, we haven't seen a big increase in filings for unemployment benefits. And the Chicago Fed estimates (using a blend of available data sources) that the unemployment rate crept up only ever so slightly in October.

November 7, 2025 at 1:34 PM

So far, we haven't seen a big increase in filings for unemployment benefits. And the Chicago Fed estimates (using a blend of available data sources) that the unemployment rate crept up only ever so slightly in October.

Start with job growth: Measures from ADP, Revelio, LinkedIn, etc., all tell subtly different stories, but they mostly agree on the big picture. After slowing dramatically over the summer, private-sector job growth has remained weak, but it hasn't necessarily slowed much further.

November 7, 2025 at 1:34 PM

Start with job growth: Measures from ADP, Revelio, LinkedIn, etc., all tell subtly different stories, but they mostly agree on the big picture. After slowing dramatically over the summer, private-sector job growth has remained weak, but it hasn't necessarily slowed much further.

Continuing claims lag by a week, so we're just beginning to see the shutdown's effect there. About 23,000 federal workers were receiving unemployment benefits as of 10/18. If you add the 10/25 claims, it'd top 30k.

November 3, 2025 at 5:22 PM

Continuing claims lag by a week, so we're just beginning to see the shutdown's effect there. About 23,000 federal workers were receiving unemployment benefits as of 10/18. If you add the 10/25 claims, it'd top 30k.

Claims from federal workers ticked down the week ending 10/25, but remain very elevated. Some historical context is important here, though -- not nearly as many claims so far as in past shutdowns. That might change as the shutdown drags on.

November 3, 2025 at 5:22 PM

Claims from federal workers ticked down the week ending 10/25, but remain very elevated. Some historical context is important here, though -- not nearly as many claims so far as in past shutdowns. That might change as the shutdown drags on.

Continuing claims continue to drift upward. That suggests that workers who lose their jobs are struggling to find news ones. Still, no sign of a dramatic deterioration since the August payroll report.

November 3, 2025 at 5:22 PM

Continuing claims continue to drift upward. That suggests that workers who lose their jobs are struggling to find news ones. Still, no sign of a dramatic deterioration since the August payroll report.

We now have unemployment claims data for all 50 states for the week ending 10/25. Still no sign of a big uptick in initial claims. (Note that these charts do NOT include federal workers -- see down thread for those.) #NumbersDay #EconSky

November 3, 2025 at 5:22 PM

We now have unemployment claims data for all 50 states for the week ending 10/25. Still no sign of a big uptick in initial claims. (Note that these charts do NOT include federal workers -- see down thread for those.) #NumbersDay #EconSky

I estimate we'll ultimately collect about $33 billion in tariff* revenue in October, a bit ahead of September's $32 billion.

* Technically this includes certain excise taxes, not only tariffs. Have to wait for the Monthly Treasury Statement for a full breakdown.

* Technically this includes certain excise taxes, not only tariffs. Have to wait for the Monthly Treasury Statement for a full breakdown.

October 24, 2025 at 8:16 PM

I estimate we'll ultimately collect about $33 billion in tariff* revenue in October, a bit ahead of September's $32 billion.

* Technically this includes certain excise taxes, not only tariffs. Have to wait for the Monthly Treasury Statement for a full breakdown.

* Technically this includes certain excise taxes, not only tariffs. Have to wait for the Monthly Treasury Statement for a full breakdown.

The Treasury has collected $31 billion in tariff revenue so far in October, and looks on track to set another monthly record.

Most analyses show that most of that money is being paid by American companies and consumers. #NumbersDay #EconSky

Most analyses show that most of that money is being paid by American companies and consumers. #NumbersDay #EconSky

October 24, 2025 at 8:14 PM

The Treasury has collected $31 billion in tariff revenue so far in October, and looks on track to set another monthly record.

Most analyses show that most of that money is being paid by American companies and consumers. #NumbersDay #EconSky

Most analyses show that most of that money is being paid by American companies and consumers. #NumbersDay #EconSky

CPI data collection issues continued in September. A record 40% of missing data was subject to "different cell" imputation, meaning the data comes from a different region.

Please see follow up tweets for some clarification of what this does and doesn't mean. #NumbersDay

Please see follow up tweets for some clarification of what this does and doesn't mean. #NumbersDay

October 24, 2025 at 3:24 PM

CPI data collection issues continued in September. A record 40% of missing data was subject to "different cell" imputation, meaning the data comes from a different region.

Please see follow up tweets for some clarification of what this does and doesn't mean. #NumbersDay

Please see follow up tweets for some clarification of what this does and doesn't mean. #NumbersDay

Unemployment is surging for Black workers — and federal government layoffs will only make it worse. Important story from @lydiadepillis.bsky.social

www.nytimes.com/2025/10/12/b... #EconSky

www.nytimes.com/2025/10/12/b... #EconSky

October 12, 2025 at 6:29 PM

Unemployment is surging for Black workers — and federal government layoffs will only make it worse. Important story from @lydiadepillis.bsky.social

www.nytimes.com/2025/10/12/b... #EconSky

www.nytimes.com/2025/10/12/b... #EconSky

The "low hire, low fire" narrative remains in place: Layoffs have edged up, but they remain low, especially when we look at a rate rather than a total number.

September 30, 2025 at 2:21 PM

The "low hire, low fire" narrative remains in place: Layoffs have edged up, but they remain low, especially when we look at a rate rather than a total number.

The quits rate has basically been bumping along for the past year or so, below its 2019 level but no longer really falling.

September 30, 2025 at 2:18 PM

The quits rate has basically been bumping along for the past year or so, below its 2019 level but no longer really falling.

The hiring rate (gross hiring, not the net job change we measure in the Friday jobs reports) has been below its long-run average for more than a year. It had seemed like it was leveling off, but might be falling again now, though hard to say definitively just yet.

September 30, 2025 at 2:17 PM

The hiring rate (gross hiring, not the net job change we measure in the Friday jobs reports) has been below its long-run average for more than a year. It had seemed like it was leveling off, but might be falling again now, though hard to say definitively just yet.

But it IS getting harder to find a job. There is now less than one job opening per unemployed worker. Not a low rate by historical standards, but definitely weaker than just before the pandemic (and way weaker than at the peak of the reopening boom).

September 30, 2025 at 2:12 PM

But it IS getting harder to find a job. There is now less than one job opening per unemployed worker. Not a low rate by historical standards, but definitely weaker than just before the pandemic (and way weaker than at the peak of the reopening boom).

A few quick #JOLTS 📈:

Starting with: Job openings are way down from their peak, but they've fallen slowly if at all in recent months. No obvious sign that labor demand is falling off a cliff.

#NumbersDay

Starting with: Job openings are way down from their peak, but they've fallen slowly if at all in recent months. No obvious sign that labor demand is falling off a cliff.

#NumbersDay

September 30, 2025 at 2:11 PM

A few quick #JOLTS 📈:

Starting with: Job openings are way down from their peak, but they've fallen slowly if at all in recent months. No obvious sign that labor demand is falling off a cliff.

#NumbersDay

Starting with: Job openings are way down from their peak, but they've fallen slowly if at all in recent months. No obvious sign that labor demand is falling off a cliff.

#NumbersDay

I'm in regular touch with people inside BLS who I'm confident would tell me if they were being pressured to change numbers.

(Are YOU a staffer at BLS or another stats agency with something I should know? Reach out!)

(Are YOU a staffer at BLS or another stats agency with something I should know? Reach out!)

September 30, 2025 at 1:42 PM

I'm in regular touch with people inside BLS who I'm confident would tell me if they were being pressured to change numbers.

(Are YOU a staffer at BLS or another stats agency with something I should know? Reach out!)

(Are YOU a staffer at BLS or another stats agency with something I should know? Reach out!)

Bottom line: Inflation is still way down from its peak. There's no sign it's taking off in a huge way. And the recent increase is in part driven by one-off factors. But it's moving in the wrong direction -- and you can no longer say "there's no sign of tariffs in the inflation data."

September 11, 2025 at 1:06 PM

Bottom line: Inflation is still way down from its peak. There's no sign it's taking off in a huge way. And the recent increase is in part driven by one-off factors. But it's moving in the wrong direction -- and you can no longer say "there's no sign of tariffs in the inflation data."

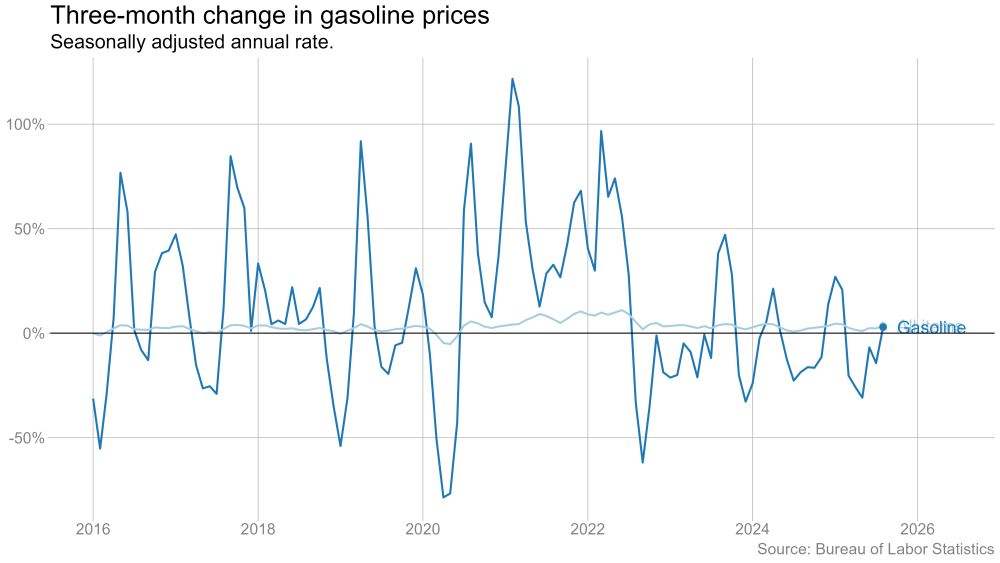

Gas prices are still down from a year earlier, but they were up from last month and are no longer falling on a three-month basis. So that's no longer a big source of relief for consumers.

September 11, 2025 at 1:02 PM

Gas prices are still down from a year earlier, but they were up from last month and are no longer falling on a three-month basis. So that's no longer a big source of relief for consumers.

You can see this clearly in this chart of core goods vs core services. Falling goods prices were key to bringing down inflation last year, but that's over now. And now services inflation is no longer cooling.

September 11, 2025 at 12:58 PM

You can see this clearly in this chart of core goods vs core services. Falling goods prices were key to bringing down inflation last year, but that's over now. And now services inflation is no longer cooling.

We had been seeing some offsetting price weakness in other categories, particularly services (perhaps suggesting consumers were cutting back elsewhere in response to higher goods prices). But that's no longer true. Check out airfares, up 5.9% in August alone.

September 11, 2025 at 12:56 PM

We had been seeing some offsetting price weakness in other categories, particularly services (perhaps suggesting consumers were cutting back elsewhere in response to higher goods prices). But that's no longer true. Check out airfares, up 5.9% in August alone.