JamesSmithRF

@jamessmithrf.bsky.social

Research Director at the Resolution Foundation. Previous lives at the Bank of England and in the civil service. Focussed mainly on macroeconomics (mainly).

Overall, today's public finances data look worrying for the govt as they suggest higher-than-expected borrowing reflects disappointing receipts and higher borrowing outside central govt. OBR cd decide that one or both of these will continue over the fcast period, increasing the fiscal blackhole.

November 21, 2025 at 9:53 AM

Overall, today's public finances data look worrying for the govt as they suggest higher-than-expected borrowing reflects disappointing receipts and higher borrowing outside central govt. OBR cd decide that one or both of these will continue over the fcast period, increasing the fiscal blackhole.

Meanwhile central government spending is just £1.4bn above forecast for the year to date (so basically in line).

November 21, 2025 at 9:53 AM

Meanwhile central government spending is just £1.4bn above forecast for the year to date (so basically in line).

So what is going on? Higher central govt borrowing is partly driven by lower receipts which are £2.8bn below forecast for Apr-Oct (hard to see on the chart, I know!). Cash receipts look better (£1.7bn above fcast) but a stronger-than-expected economy should mean *stronger* receipts than the OBR had.

November 21, 2025 at 9:53 AM

So what is going on? Higher central govt borrowing is partly driven by lower receipts which are £2.8bn below forecast for Apr-Oct (hard to see on the chart, I know!). Cash receipts look better (£1.7bn above fcast) but a stronger-than-expected economy should mean *stronger* receipts than the OBR had.

So borrowing was above the OBR's forecast by £3.1bn in Oct. The chart shows borrowing £9.9bn above fcast for the year to date at £116.8bn- keep in mind, OBR fcast for borrowing for the whole year is £117.7bn. Only £4.2bn is central govt tho, with Local Auth and Pub Corps accounting for the rest.

November 21, 2025 at 9:53 AM

So borrowing was above the OBR's forecast by £3.1bn in Oct. The chart shows borrowing £9.9bn above fcast for the year to date at £116.8bn- keep in mind, OBR fcast for borrowing for the whole year is £117.7bn. Only £4.2bn is central govt tho, with Local Auth and Pub Corps accounting for the rest.

So the inflation outlook feels a bit better this morning with the peak seemingly behind us. If the Chancellor can help with the cost of living at the Budget it should help accelerate the fall and should give room for the BoE to deliver much needed rate cuts.

November 19, 2025 at 8:29 AM

So the inflation outlook feels a bit better this morning with the peak seemingly behind us. If the Chancellor can help with the cost of living at the Budget it should help accelerate the fall and should give room for the BoE to deliver much needed rate cuts.

Finally, underlying inflation pressures look a bit better in this release with services inflation falling further (left chart) and, at a high frequency, this measure (right chart) now looks consistent (if not below) levels consistent with meeting the 2% target in the past.

November 19, 2025 at 8:29 AM

Finally, underlying inflation pressures look a bit better in this release with services inflation falling further (left chart) and, at a high frequency, this measure (right chart) now looks consistent (if not below) levels consistent with meeting the 2% target in the past.

The Chancellor should act on the cost of living at next week's Budget. Best way to do that is to remove some the costs of government policies that are put on electricity bills from bills and instead paying for them via general taxation. See: www.resolutionfoundation.org/publications...

Splitting the bill • Resolution Foundation

This note looks at the factors behind stubbornly high energy bills and how ministers could act to ease pressure on households. It considers how change can be enacted to work for vulnerable families an...

www.resolutionfoundation.org

November 19, 2025 at 8:29 AM

The Chancellor should act on the cost of living at next week's Budget. Best way to do that is to remove some the costs of government policies that are put on electricity bills from bills and instead paying for them via general taxation. See: www.resolutionfoundation.org/publications...

This high cost of essential is still showing up in measures of hardship. Foodbank use is still very high (left chart) and energy-related debts are continuing to rise (right chart).

November 19, 2025 at 8:29 AM

This high cost of essential is still showing up in measures of hardship. Foodbank use is still very high (left chart) and energy-related debts are continuing to rise (right chart).

The combination of high energy prices and rising food costs come against a backdrop of shift higher in the cost of essentials (left chart). This is particularly bad news for the lowest-income families who spend about a third more on such essentials than the highest-income families (right chart).

November 19, 2025 at 8:29 AM

The combination of high energy prices and rising food costs come against a backdrop of shift higher in the cost of essentials (left chart). This is particularly bad news for the lowest-income families who spend about a third more on such essentials than the highest-income families (right chart).

Changes on the month, are all about energy prices. While energy prices were up in October (the Ofgem price cap increased by £35 to £1,755), rises a year ago fell out of the 12-month calculation. Food price inflation picked up again too - rising to 4.9% in Oct (from 4.5% in Sep).

November 19, 2025 at 8:29 AM

Changes on the month, are all about energy prices. While energy prices were up in October (the Ofgem price cap increased by £35 to £1,755), rises a year ago fell out of the 12-month calculation. Food price inflation picked up again too - rising to 4.9% in Oct (from 4.5% in Sep).

UK CPI inflation fell 0.2ppts to 3.6% in October, in line with BoE expectations (but slightly above market consensus of 3.5%). BoE says inflation has peaked and will drift down. This chart reminds you that UK inflation is still higher than elsewhere with administered prices adding 0.4ppts to CPI.

November 19, 2025 at 8:29 AM

UK CPI inflation fell 0.2ppts to 3.6% in October, in line with BoE expectations (but slightly above market consensus of 3.5%). BoE says inflation has peaked and will drift down. This chart reminds you that UK inflation is still higher than elsewhere with administered prices adding 0.4ppts to CPI.

Overall, then, this is a disappointing GDP release with another second-half of the year slowdown in evidence. Growth is, at best, stodgy, reinforcing the stagnation challenges face. The good news for the Chancellor is that this this release comes too late for the OBR forecasts!

November 13, 2025 at 8:49 AM

Overall, then, this is a disappointing GDP release with another second-half of the year slowdown in evidence. Growth is, at best, stodgy, reinforcing the stagnation challenges face. The good news for the Chancellor is that this this release comes too late for the OBR forecasts!

GDP per person (which tracks living standards more closely) was flat in Q3 and has grown at an annualised rate of just 0.8% over the Parliament so far. This is stronger than post-GFC avg of 0.6% but weaker than the 2010s avg of 1.3% per cent, and well below 1993-2008 avg of 2.5%.

November 13, 2025 at 8:49 AM

GDP per person (which tracks living standards more closely) was flat in Q3 and has grown at an annualised rate of just 0.8% over the Parliament so far. This is stronger than post-GFC avg of 0.6% but weaker than the 2010s avg of 1.3% per cent, and well below 1993-2008 avg of 2.5%.

Looking at expenditure, the picture is...confusing! Growth in Q3 is largely driven by investment (although not from business, which fell on the quarter!). The (poss) good news is ONS can find more expenditure than output, suggesting scope for revisions. Concerningly, consumption remains weak.

November 13, 2025 at 8:49 AM

Looking at expenditure, the picture is...confusing! Growth in Q3 is largely driven by investment (although not from business, which fell on the quarter!). The (poss) good news is ONS can find more expenditure than output, suggesting scope for revisions. Concerningly, consumption remains weak.

You can see the slowing more clearly in the monthly data with output contracting in September. Looking at sectors, there was an encouraging bounce back in services in Sep offset by very weak production, affected by weak car production (affected by Jaguar outage).

November 13, 2025 at 8:49 AM

You can see the slowing more clearly in the monthly data with output contracting in September. Looking at sectors, there was an encouraging bounce back in services in Sep offset by very weak production, affected by weak car production (affected by Jaguar outage).

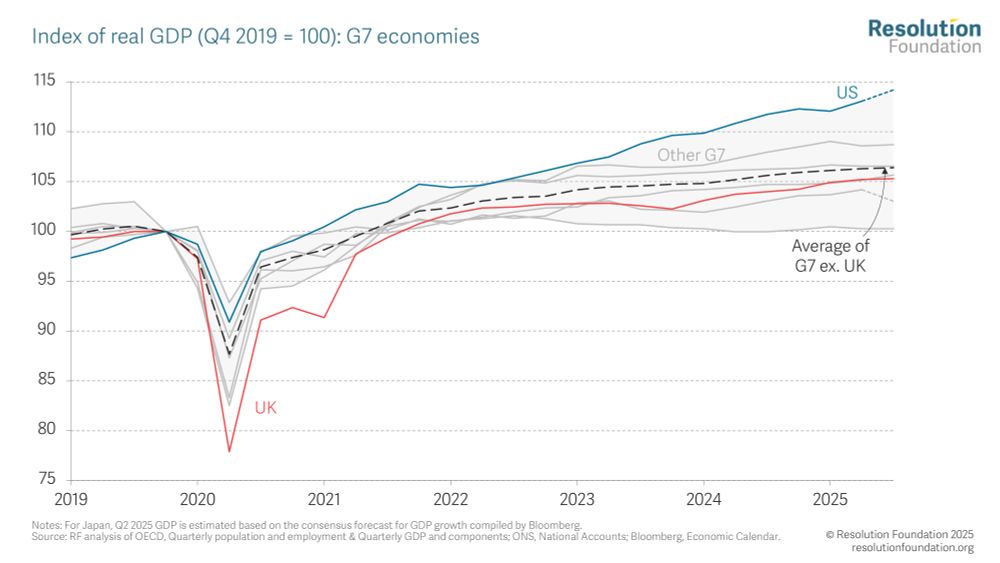

If you look at growth relative to other rich countries, the UK looks mid-table for Q3 (although this comparison is made trickier by delays to US publication). Stepping back, the has been the second fastest growing G7 economy in the first 9 months of 2025- still decent growth by recent standards.

November 13, 2025 at 8:49 AM

If you look at growth relative to other rich countries, the UK looks mid-table for Q3 (although this comparison is made trickier by delays to US publication). Stepping back, the has been the second fastest growing G7 economy in the first 9 months of 2025- still decent growth by recent standards.

So growth slowed to a disappointing 0.1% in Q3 - this is *another* year (after 2023 and 2024) in which growth has slowed in the second half of the year after a promising start. Growth in Q3 was way below the post-pandemic normal (which itself is very weak!).

November 13, 2025 at 8:49 AM

So growth slowed to a disappointing 0.1% in Q3 - this is *another* year (after 2023 and 2024) in which growth has slowed in the second half of the year after a promising start. Growth in Q3 was way below the post-pandemic normal (which itself is very weak!).