Andrew Granato

@agranato42.bsky.social

PhD candidate in financial economics at Yale; JD ‘24. "We are selling to willing buyers at the current fair market price - so that we may survive." Site: https://sites.google.com/view/andrewgranato/

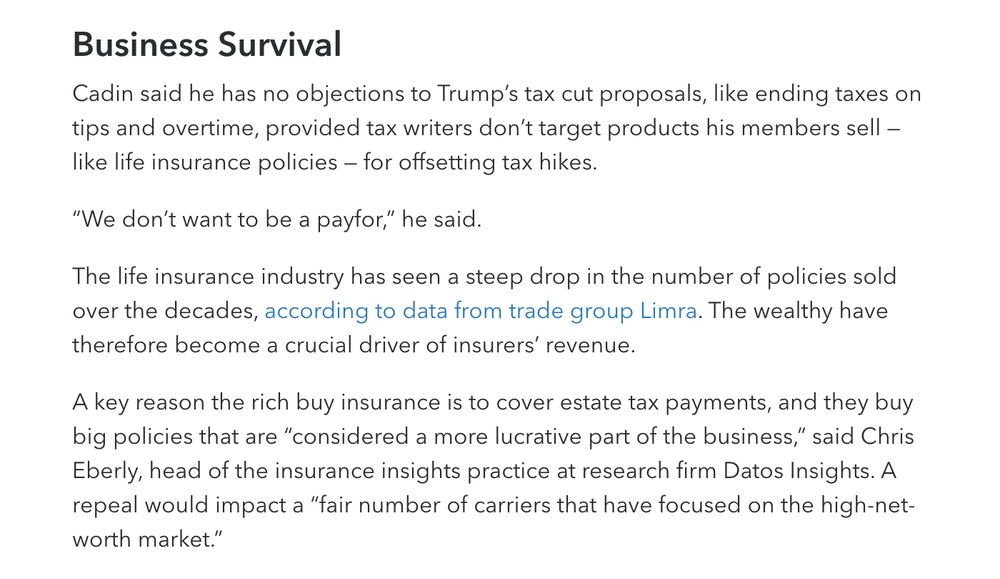

I'm quoted in the latest @laurenloricchio.bsky.social + @chandrawallace.bsky.social @taxnotes.com investigation of the "offshore" life insurance industry, which found a Russian oligarch with a $430 million policy. Article here: www.taxnotes.com/tax-notes-to...

November 24, 2025 at 11:04 PM

I'm quoted in the latest @laurenloricchio.bsky.social + @chandrawallace.bsky.social @taxnotes.com investigation of the "offshore" life insurance industry, which found a Russian oligarch with a $430 million policy. Article here: www.taxnotes.com/tax-notes-to...

I am on the legal academic job market! My job talk paper is on how courts in tax, corporate, and bankruptcy law spheres value business interests systematically differently, such that the same asset is "worth" different amounts of money depending on the substantive underlying law.

August 12, 2025 at 3:48 PM

I am on the legal academic job market! My job talk paper is on how courts in tax, corporate, and bankruptcy law spheres value business interests systematically differently, such that the same asset is "worth" different amounts of money depending on the substantive underlying law.

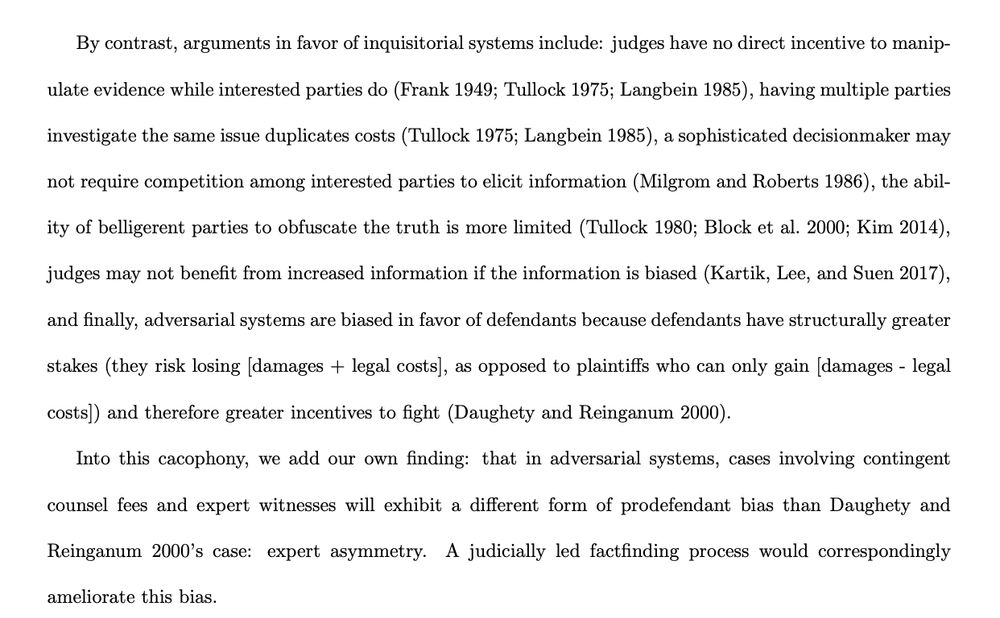

We argue that expert asymmetry provides another potential justification for "inquisitorial" over "adversarial" litigation procedures, specifically increased judicial deployment of Federal Rule of Evidence 706, which permits judicially appointed experts.

June 18, 2025 at 2:50 PM

We argue that expert asymmetry provides another potential justification for "inquisitorial" over "adversarial" litigation procedures, specifically increased judicial deployment of Federal Rule of Evidence 706, which permits judicially appointed experts.

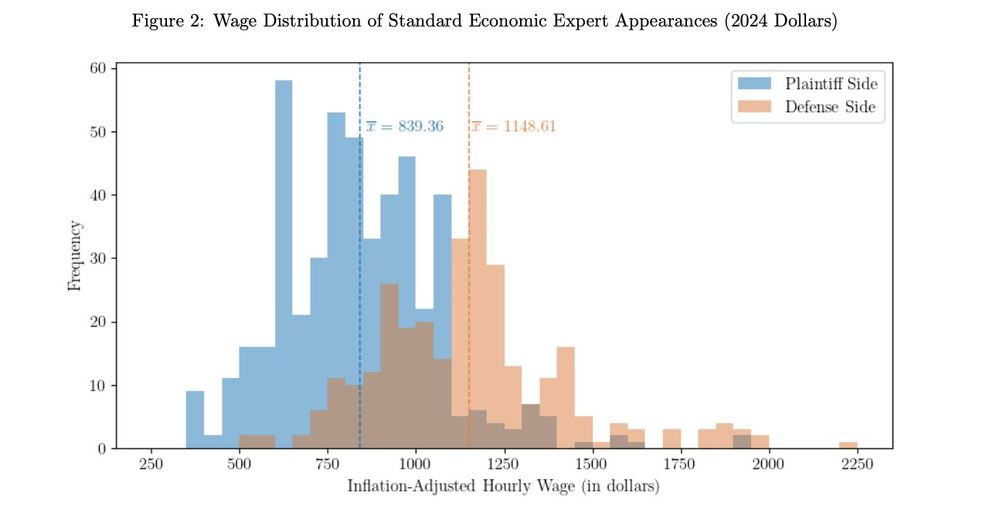

Adjusting for inflation, the plaintiff-side economic experts (performing mostly 'event studies') are paid an average of $840 an hour in securities litigation, while the defense-side economic experts are paid an average of $1,150 an hour.

June 18, 2025 at 2:50 PM

Adjusting for inflation, the plaintiff-side economic experts (performing mostly 'event studies') are paid an average of $840 an hour in securities litigation, while the defense-side economic experts are paid an average of $1,150 an hour.

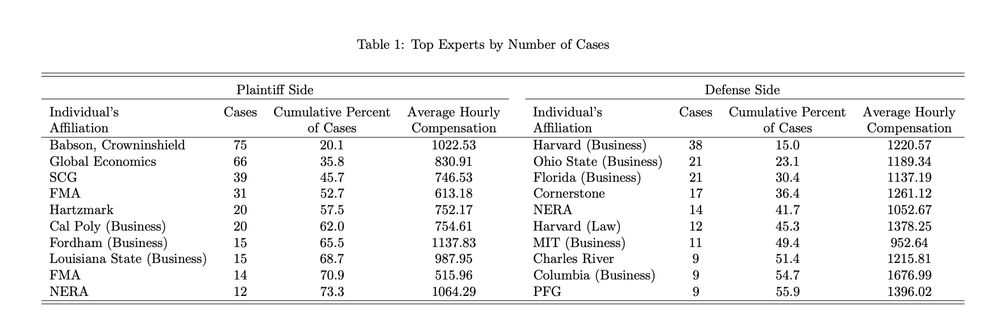

We test our complete model in securities litigation. Experts (at the individual and consulting firm level) polarize into almost entirely plaintiff-side vs. defense-side experts who are repeat players. Roughly 20 people appears in outright majorities of cases in this field.

June 18, 2025 at 2:50 PM

We test our complete model in securities litigation. Experts (at the individual and consulting firm level) polarize into almost entirely plaintiff-side vs. defense-side experts who are repeat players. Roughly 20 people appears in outright majorities of cases in this field.

In the simple case, this is a pure agency issue, which we model. But civil procedure law also provides for an litigation expense reimbursement out of class winnings if the plaintiff wins, meaning that which party has incentive to spend more on experts is not initially clear!

June 18, 2025 at 2:50 PM

In the simple case, this is a pure agency issue, which we model. But civil procedure law also provides for an litigation expense reimbursement out of class winnings if the plaintiff wins, meaning that which party has incentive to spend more on experts is not initially clear!

In class actions, as well as in many individual suits, plaintiffs' attorneys are compensated on contingency (they get a % of winnings if they win/settle, but get $0 if they lose), but they have to pay for litigation expenses (including experts) upfront.

June 18, 2025 at 2:50 PM

In class actions, as well as in many individual suits, plaintiffs' attorneys are compensated on contingency (they get a % of winnings if they win/settle, but get $0 if they lose), but they have to pay for litigation expenses (including experts) upfront.

The idea: expert witnesses are ubiquitous across law (antitrust! patent! toxic torts!), but no studies empirically study the use of expert witnesses at scale. We do so in securities litigation, which is more familiar to us as business scholars + docket data is more accessible.

June 18, 2025 at 2:50 PM

The idea: expert witnesses are ubiquitous across law (antitrust! patent! toxic torts!), but no studies empirically study the use of expert witnesses at scale. We do so in securities litigation, which is more familiar to us as business scholars + docket data is more accessible.

NEW PAPER: Expert Asymmetry. When there is a "battle of the experts," civil procedure rules mean that defendants spend more on expert witnesses. In a decade of handcollected securities litigation data, Ds spend 37% more on economist experts (avg $1,150/hour). Draft: papers.ssrn.com/sol3/papers....

June 18, 2025 at 2:50 PM

NEW PAPER: Expert Asymmetry. When there is a "battle of the experts," civil procedure rules mean that defendants spend more on expert witnesses. In a decade of handcollected securities litigation data, Ds spend 37% more on economist experts (avg $1,150/hour). Draft: papers.ssrn.com/sol3/papers....

Securities class actions are an effective place to study civil procedure because they are tracked, fairly standardized, and nearly always filed in federal courts so their Dockets are available on Bloomberg. scholarlycommons.law.emory.edu/cgi/viewcont...

June 8, 2025 at 11:57 PM

Securities class actions are an effective place to study civil procedure because they are tracked, fairly standardized, and nearly always filed in federal courts so their Dockets are available on Bloomberg. scholarlycommons.law.emory.edu/cgi/viewcont...

now this is a fun one academic.oup.com/jla/article/...

June 1, 2025 at 10:20 PM

now this is a fun one academic.oup.com/jla/article/...

There could always be a substance over form challenge, and the fact that this 351-ETF idea is pretty novel when the applicable regs have been around since 1996 suggests to me that there's hesitance about doing something that's intuitively against the spirit of 351, but there's a textual basis there.

June 1, 2025 at 12:59 PM

There could always be a substance over form challenge, and the fact that this 351-ETF idea is pretty novel when the applicable regs have been around since 1996 suggests to me that there's hesitance about doing something that's intuitively against the spirit of 351, but there's a textual basis there.

W/caveats that I'm just reading the regs directly and may be missing outside context, it's structured to qualify as a 351 under 1.351-1(c)(6)'s exception. 1(c)(6)'s modification of "diversification" should also help resolve problems with the last sentence of 1(c)(5), which would otherwise doom it.

June 1, 2025 at 12:59 PM

W/caveats that I'm just reading the regs directly and may be missing outside context, it's structured to qualify as a 351 under 1.351-1(c)(6)'s exception. 1(c)(6)'s modification of "diversification" should also help resolve problems with the last sentence of 1(c)(5), which would otherwise doom it.

An ETF company, Alpha Architects, is about to launch a product specifically designed so that high-net-worth investors with relatively concentrated portfolios and high unrealized gains can conduct a tax-free 351 transfer into a fully diversified ETF. funds.alphaarchitect.com/wp-content/u...

May 31, 2025 at 6:24 PM

An ETF company, Alpha Architects, is about to launch a product specifically designed so that high-net-worth investors with relatively concentrated portfolios and high unrealized gains can conduct a tax-free 351 transfer into a fully diversified ETF. funds.alphaarchitect.com/wp-content/u...

Thanks to ICI Research Seminar for having me to talk about life insurance taxation. More to come!

April 25, 2025 at 9:18 PM

Thanks to ICI Research Seminar for having me to talk about life insurance taxation. More to come!

What’s inconvenient? Flying in and out of an airport half a state away when there’s an airport with a similar route in your very city. What’s the right thing to do? Refuse to support an airport that volunteers for lawless ICE deportation flights. Proud to boycott Avelo. www.wfsb.com/2025/04/17/p...

April 24, 2025 at 5:50 PM

What’s inconvenient? Flying in and out of an airport half a state away when there’s an airport with a similar route in your very city. What’s the right thing to do? Refuse to support an airport that volunteers for lawless ICE deportation flights. Proud to boycott Avelo. www.wfsb.com/2025/04/17/p...

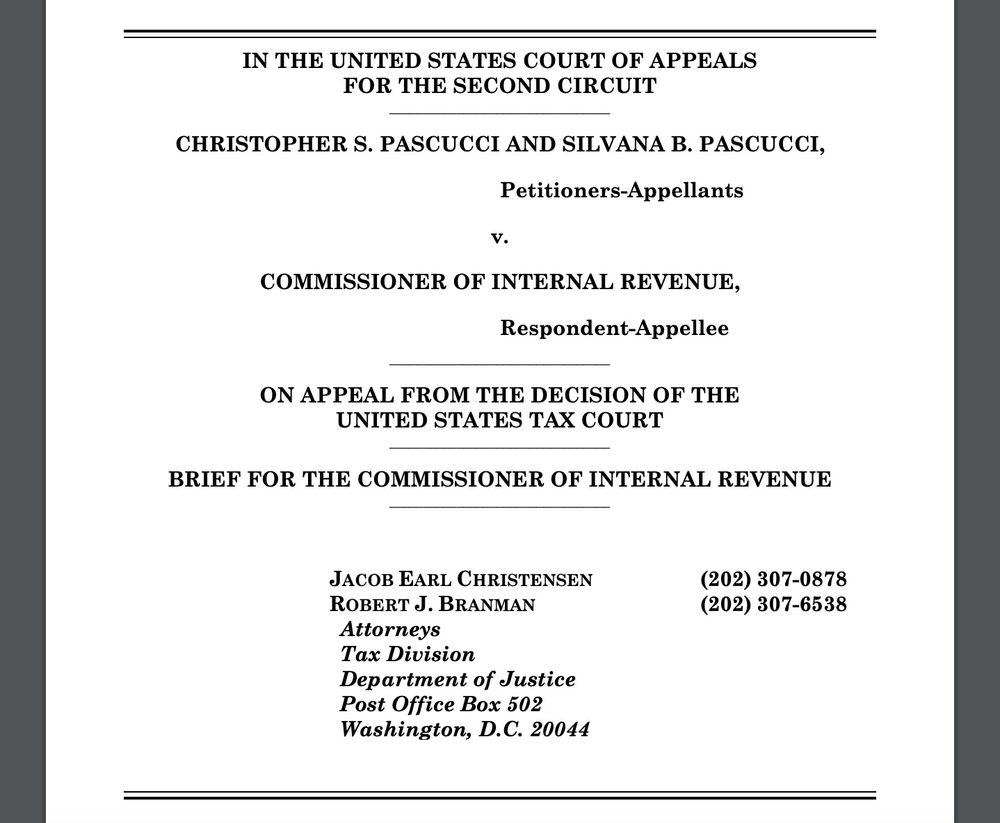

The Department of Justice has cited my life insurance tax article with Ari Glogower in the appeal of this case in the Second Circuit. The case flips the usual sides on which party, the IRS or the taxpayer, wants to say who violated the investor control doctrine. www.bloomberglaw.com/product/blaw...

March 5, 2025 at 3:52 PM

The Department of Justice has cited my life insurance tax article with Ari Glogower in the appeal of this case in the Second Circuit. The case flips the usual sides on which party, the IRS or the taxpayer, wants to say who violated the investor control doctrine. www.bloomberglaw.com/product/blaw...

Happy Awad v. AMC Entertainment Holdings, Inc. day to all who celebrate

February 21, 2025 at 7:01 PM

Happy Awad v. AMC Entertainment Holdings, Inc. day to all who celebrate

A paper I have been thinking about a lot is @gelbach.bsky.social's Beyond Transsubstantivity, in which he uses docket data from 500k cases to show that antitrust, patent, environmental tort, and securities cases are the most complex using several different metrics. papers.ssrn.com/sol3/papers....

January 26, 2025 at 10:34 PM

A paper I have been thinking about a lot is @gelbach.bsky.social's Beyond Transsubstantivity, in which he uses docket data from 500k cases to show that antitrust, patent, environmental tort, and securities cases are the most complex using several different metrics. papers.ssrn.com/sol3/papers....

as I work up notes for gift & estate tax it occurs to me that given that this is the definition of a person's "gross estate," I'm shocked we don't see more controversy about the definitions used for 'wealth' when measuring wealth inequality

December 14, 2024 at 2:43 AM

as I work up notes for gift & estate tax it occurs to me that given that this is the definition of a person's "gross estate," I'm shocked we don't see more controversy about the definitions used for 'wealth' when measuring wealth inequality

I would like to thank the YLS law & economics paper prize committee for their recognition of my work on the outcomes of law firm "partner runs" and their implications for law firm organizational form. Updated version coming in future months!

December 2, 2024 at 9:33 PM

I would like to thank the YLS law & economics paper prize committee for their recognition of my work on the outcomes of law firm "partner runs" and their implications for law firm organizational form. Updated version coming in future months!

[to the tune of We Didn't Start the Fire]

November 27, 2024 at 11:27 PM

[to the tune of We Didn't Start the Fire]