Steve Markus

@stevem1.bsky.social

Chesterfield UK based Investor, like small caps and general industrials. Fundies based on the whole, like to buy and hold. Background in management consulting and software/database tech across the development and implementation lifecycle.

Michelmersh Brick #MBH.L FY TU, trading/profitability ahead of H1 but seen a notable slowdown in construction activity in Q4, mention Budget. Revenue and adj EBITDA of £69M and £12.5M respectively, a little below expectations altho they don't say so. More settled production, positive order intake.

December 2, 2025 at 7:20 AM

Michelmersh Brick #MBH.L FY TU, trading/profitability ahead of H1 but seen a notable slowdown in construction activity in Q4, mention Budget. Revenue and adj EBITDA of £69M and £12.5M respectively, a little below expectations altho they don't say so. More settled production, positive order intake.

Solid State #SOLI.L H1 results look ok, confident of full year in line and a big improvement on previous yr. Overshadowed by death of previous CEO Gary Marsh. Order book at £97M on 30 Nov (H1 24/25 £76.6M). Suffered from lumpy contracts last yr and could so again but seems to be recovering ok.

December 1, 2025 at 7:25 AM

Solid State #SOLI.L H1 results look ok, confident of full year in line and a big improvement on previous yr. Overshadowed by death of previous CEO Gary Marsh. Order book at £97M on 30 Nov (H1 24/25 £76.6M). Suffered from lumpy contracts last yr and could so again but seems to be recovering ok.

Iomart #IOM.L interims, new management and acquisitions do not appear to have changed the overall direction, although they claim that H2 will be better and full year to be within the range of current market expectations. Has always been a sinking company in a buoyant sector.

November 26, 2025 at 7:24 AM

Iomart #IOM.L interims, new management and acquisitions do not appear to have changed the overall direction, although they claim that H2 will be better and full year to be within the range of current market expectations. Has always been a sinking company in a buoyant sector.

Cranswick #CWK.L interims are a thing of beauty (apart from debt, up and explained by acquisition, capex and working capital). Outlook for full year in line with expectations. Continues their history of reliable delivery.

November 25, 2025 at 7:36 AM

Cranswick #CWK.L interims are a thing of beauty (apart from debt, up and explained by acquisition, capex and working capital). Outlook for full year in line with expectations. Continues their history of reliable delivery.

Renew #RNWH.L finals pretty much as expected, revenue up 5.6%, adj EPS 67.1p (65.9), full yr divi 20p. Seem to have used the slack rail period to restructure, in a better position for remainder of CP7. Record order book moving into 2026, 'the foundations of the business have never been stronger'

November 25, 2025 at 7:16 AM

Renew #RNWH.L finals pretty much as expected, revenue up 5.6%, adj EPS 67.1p (65.9), full yr divi 20p. Seem to have used the slack rail period to restructure, in a better position for remainder of CP7. Record order book moving into 2026, 'the foundations of the business have never been stronger'

Treatt #TET.L newish CEO David Shannon stepping down as CEO and from Board, thanked. Unsurprising given the recent poor performance and seeming capitulation to lowball takeovers.

November 25, 2025 at 7:09 AM

Treatt #TET.L newish CEO David Shannon stepping down as CEO and from Board, thanked. Unsurprising given the recent poor performance and seeming capitulation to lowball takeovers.

TT Electronics #TTG.L October TU, tentative with full year expected in line but requires 'siggnificant step up' in November and December, relies on expected order delivery times. 2026 difficult to predict but currently seen as flattish on 2025, but without the one-offs. Slightly down then.

November 24, 2025 at 7:21 AM

TT Electronics #TTG.L October TU, tentative with full year expected in line but requires 'siggnificant step up' in November and December, relies on expected order delivery times. 2026 difficult to predict but currently seen as flattish on 2025, but without the one-offs. Slightly down then.

#IMI.L agreed the sale of their Truflo Marine division 'further aligns IMI to three powerful growth trends - energy, automation and healthcare'. Looks like a decent price.

November 24, 2025 at 7:10 AM

#IMI.L agreed the sale of their Truflo Marine division 'further aligns IMI to three powerful growth trends - energy, automation and healthcare'. Looks like a decent price.

Babcock #BAB.L H1 results look good, EPS 33.7p (25.7p), divi 2.5p (2.0p), net debt excluding leases £55.8M (145.8M). Outlook for FY 2026 inline and 'pursuing exciting opportunities for sustainable growth and margin expansion, both in the UK and internationally'. Quite a turnround from a few yrs ago.

November 21, 2025 at 7:38 AM

Babcock #BAB.L H1 results look good, EPS 33.7p (25.7p), divi 2.5p (2.0p), net debt excluding leases £55.8M (145.8M). Outlook for FY 2026 inline and 'pursuing exciting opportunities for sustainable growth and margin expansion, both in the UK and internationally'. Quite a turnround from a few yrs ago.

Norcros #NXR.L interims look ok, underlying operating profit up 7%, revenue up 1.3, debt down to £30.7M (44.9M). In line for full year, acquisition of Fibo in Norway to be earnings enhancing. Looks good and growth in earnings nice to see.

November 20, 2025 at 7:33 AM

Norcros #NXR.L interims look ok, underlying operating profit up 7%, revenue up 1.3, debt down to £30.7M (44.9M). In line for full year, acquisition of Fibo in Norway to be earnings enhancing. Looks good and growth in earnings nice to see.

Tracsis #TRCS.L finals look ok but heavily adjusted, 24.8p eps turns into 1.7p basic! Results flattish but ok, plus has £23.4M net cash. Waiting for UK Rail to sort themselves out, looking for acquisitions. Q1 in line, full yr adj EBITDA in line (and is slightly higher at £13-13.8M).

November 20, 2025 at 7:27 AM

Tracsis #TRCS.L finals look ok but heavily adjusted, 24.8p eps turns into 1.7p basic! Results flattish but ok, plus has £23.4M net cash. Waiting for UK Rail to sort themselves out, looking for acquisitions. Q1 in line, full yr adj EBITDA in line (and is slightly higher at £13-13.8M).

Solid State #SOLI.L announcing several major orders for specialist power packs for Custom Power subsidiary worth $7.4M, both new and repeat business. Custom Power had shown promise but not been outstanding, so good news. I bought #SOLI on TU a couple of weeks ago, pleased to see this.

November 20, 2025 at 7:11 AM

Rotork #ROR.L TU, full year expectations unchanged, new £50M buyback announced and they can afford it with £37.3M net cash. Group order intake 8% higher YoY including Noah acqn, overall end markets remain supportive. Another niche engineer doing well.

November 19, 2025 at 7:37 AM

Rotork #ROR.L TU, full year expectations unchanged, new £50M buyback announced and they can afford it with £37.3M net cash. Group order intake 8% higher YoY including Noah acqn, overall end markets remain supportive. Another niche engineer doing well.

Likeise #LIKE.L TU, blow own trumpet loudly regarding revenue growth of 8.9% YTD but fails to recognise that turnover is vanity and profits sanity and tells us that underlying PBT is going to fall short of expectations. Still going to be 'significantly ahead' of previous years though. Oops.

November 19, 2025 at 7:26 AM

Likeise #LIKE.L TU, blow own trumpet loudly regarding revenue growth of 8.9% YTD but fails to recognise that turnover is vanity and profits sanity and tells us that underlying PBT is going to fall short of expectations. Still going to be 'significantly ahead' of previous years though. Oops.

Hill & Smith #HILS.L TU, FY in line with expectations, US Engineered Solutions offsetting weaker UK and India, Galvanising showing volume growth in both UK and US. Expect progress on Group margins. Cash generation continued to be good, has always been a feature of HILS. One of my favourites.

November 19, 2025 at 7:18 AM

Hill & Smith #HILS.L TU, FY in line with expectations, US Engineered Solutions offsetting weaker UK and India, Galvanising showing volume growth in both UK and US. Expect progress on Group margins. Cash generation continued to be good, has always been a feature of HILS. One of my favourites.

Zotefoams #ZTF.L has acquired a Spanish technical foams co, Overseas Konstellation Company, for Eu27.6M initial plus up to Eu8.4M earnout. Earnings accretive in the first full yr, a lot of info in the RNS about strategic fit re markets and geography, looks well thought through and a decent acqn.

November 18, 2025 at 3:50 PM

Zotefoams #ZTF.L has acquired a Spanish technical foams co, Overseas Konstellation Company, for Eu27.6M initial plus up to Eu8.4M earnout. Earnings accretive in the first full yr, a lot of info in the RNS about strategic fit re markets and geography, looks well thought through and a decent acqn.

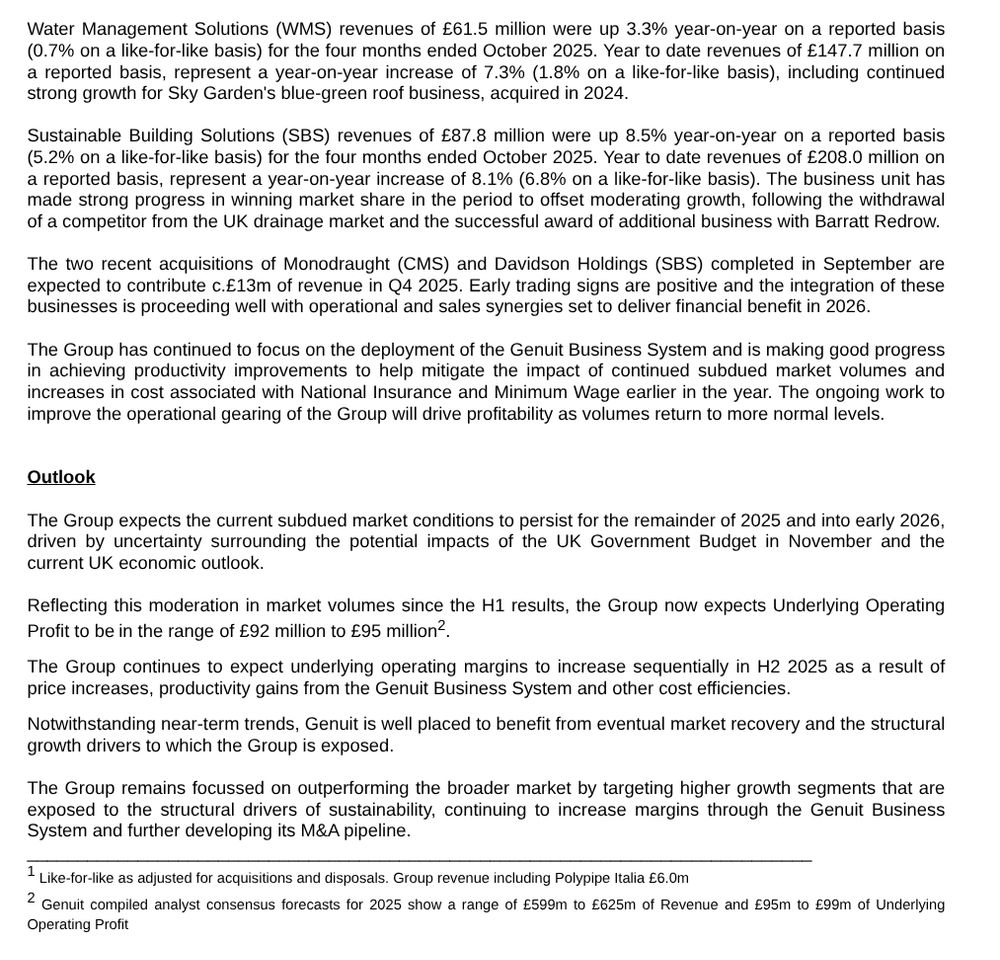

Genuit #GEN.L hit by the curse of slow RMI, now expects adj operating profit in raange £92M-95M (was £95-99M). Revenue up 8.4% so margins must have declined although not clear in which area. the recent couple of acquisitions showing positive early trading signs. Conditions to persist into early 2026

November 17, 2025 at 7:28 AM

Genuit #GEN.L hit by the curse of slow RMI, now expects adj operating profit in raange £92M-95M (was £95-99M). Revenue up 8.4% so margins must have declined although not clear in which area. the recent couple of acquisitions showing positive early trading signs. Conditions to persist into early 2026

Stelrad #SRAD.L FY TU, bit lukewarm due to a subdued market for radiators, now expect FY adjusted operating profit between £32M and £33M, up on previous year with margins better, but looks a bit below expectations. Expect debt to improve, have been improving Turkish business at a cost of £1.6M.

November 17, 2025 at 7:13 AM

Stelrad #SRAD.L FY TU, bit lukewarm due to a subdued market for radiators, now expect FY adjusted operating profit between £32M and £33M, up on previous year with margins better, but looks a bit below expectations. Expect debt to improve, have been improving Turkish business at a cost of £1.6M.

Gleeson #GLE.L AGM TU, unexciting but steady, expects FY26 results to be in line with expectations but mindful of Autumn Budget, seeing some progress with reservation rates up on the same period YoY. One significant land sale still waiting for a technical solution

November 14, 2025 at 7:26 AM

Gleeson #GLE.L AGM TU, unexciting but steady, expects FY26 results to be in line with expectations but mindful of Autumn Budget, seeing some progress with reservation rates up on the same period YoY. One significant land sale still waiting for a technical solution

Melrose #MRO.L Q3 TU reads well, in line with full year expectations and Engines revenue up 28% with record backlogs, Structures up 5% helped by defence demand. A long way from GKN days.

November 14, 2025 at 7:20 AM

Melrose #MRO.L Q3 TU reads well, in line with full year expectations and Engines revenue up 28% with record backlogs, Structures up 5% helped by defence demand. A long way from GKN days.

Aviva #AV.L Q3 TU, on track to achieve 2026 targets a year early, Amanda Blanc 'the outlook for Aviva has never been better'. Upgrading savings from Direct Line acquisition, setting new 3 year targets. Reads very well.

November 13, 2025 at 7:41 AM

Aviva #AV.L Q3 TU, on track to achieve 2026 targets a year early, Amanda Blanc 'the outlook for Aviva has never been better'. Upgrading savings from Direct Line acquisition, setting new 3 year targets. Reads very well.

Convatec #CTEC.L 10 month TU, full yr 2025 in line, expecting 2026 to be another year of double-digit adjusted EPS growth. Some ongoing regulatory difficulties for product Innovamatrix, but not holding back growth. New CEO and CFO following unfortunate death thru illness of previous CEO Karim Bitar.

November 13, 2025 at 7:27 AM

Convatec #CTEC.L 10 month TU, full yr 2025 in line, expecting 2026 to be another year of double-digit adjusted EPS growth. Some ongoing regulatory difficulties for product Innovamatrix, but not holding back growth. New CEO and CFO following unfortunate death thru illness of previous CEO Karim Bitar.

Keller #KLR.L Q3 TU, confirming in line for full yr, Asia-Pacific performance 'robust', everywhere else seems fairly solid. Approaching net cash position by end of year. Record level order book, geographic diversity give visibility and resilience. Happy as a long term holder.

November 13, 2025 at 7:14 AM

Keller #KLR.L Q3 TU, confirming in line for full yr, Asia-Pacific performance 'robust', everywhere else seems fairly solid. Approaching net cash position by end of year. Record level order book, geographic diversity give visibility and resilience. Happy as a long term holder.

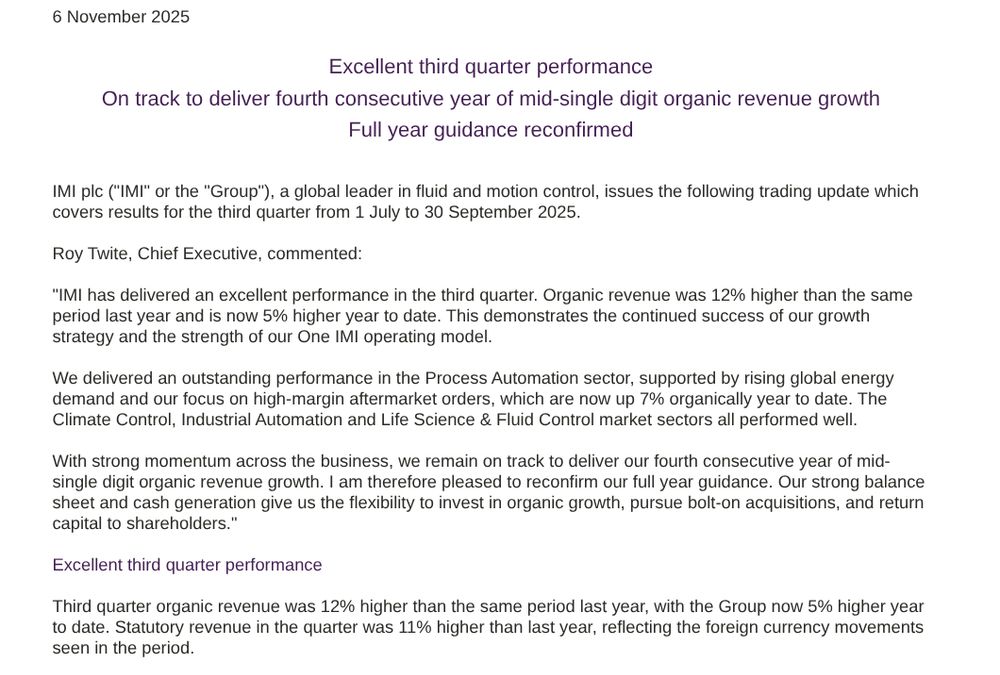

#IMI.L Q3 TU, plenty of repetitions of excellent, reads well. On track for full year expectations of mid single-digit growth and adj eps between 129 and 135p. Process Automation doing particularly well with revenue up 14%YTD and 26% in Q3.

November 6, 2025 at 7:13 AM

#IMI.L Q3 TU, plenty of repetitions of excellent, reads well. On track for full year expectations of mid single-digit growth and adj eps between 129 and 135p. Process Automation doing particularly well with revenue up 14%YTD and 26% in Q3.