Jason Furman

@jasonfurman.bsky.social

Professor at Harvard. Teaches Ec 10, some posts might be educational. Also Senior Fellow @PIIE.com & contributor

@nytopinion.nytimes.com. Was Chair of President Obama's CEA.

@nytopinion.nytimes.com. Was Chair of President Obama's CEA.

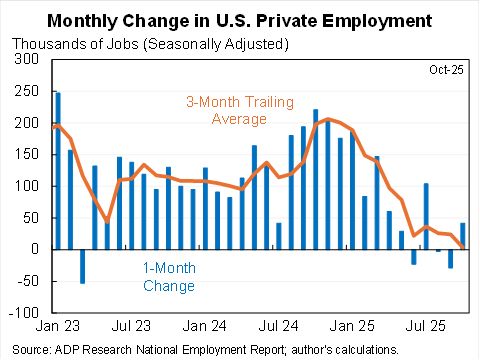

Jobs numbers, per ADP. Back in the black but not by much--and 3-month moving average basically zero.

November 5, 2025 at 2:57 PM

Jobs numbers, per ADP. Back in the black but not by much--and 3-month moving average basically zero.

If average work hours per person fall dramatically in the future due to AI is that more likely to be because:

1. AI substitutes for labor, market-clearing wage falls below zero, people not hired.

2. AI complements labor, wages rise, income effects so people don't work as much.

1. AI substitutes for labor, market-clearing wage falls below zero, people not hired.

2. AI complements labor, wages rise, income effects so people don't work as much.

November 4, 2025 at 10:12 PM

If average work hours per person fall dramatically in the future due to AI is that more likely to be because:

1. AI substitutes for labor, market-clearing wage falls below zero, people not hired.

2. AI complements labor, wages rise, income effects so people don't work as much.

1. AI substitutes for labor, market-clearing wage falls below zero, people not hired.

2. AI complements labor, wages rise, income effects so people don't work as much.

Reposted by Jason Furman

I am also ranking Burhan Azeem as my #1 choice. I agree with everything Josh says. And I've also personally been really impressed with Burhan's amazing combination of commitment to Cambridge, deep thoughtfulness about the issues it faces and pragmatism and inclusiveness in his approach to them.

I'll shortly write a longer post, but I just wanted to say that I'm ranking Burhan Azeem as my #1 City Council choice, largely because of his relentless and successful push to fix our city's housing policy (largely by eliminating zoning restrictions that drive up rents and sales prices).

For the first time in a generation, triple-deckers and affordable apartments are legal again in Cambridge.

Impossible? It wasn’t.

Inevitable? It’s wasn’t that either.

It was a choice.

Vote Burhan #1 on Nov 4th and keep choosing housing.

Impossible? It wasn’t.

Inevitable? It’s wasn’t that either.

It was a choice.

Vote Burhan #1 on Nov 4th and keep choosing housing.

November 3, 2025 at 6:19 PM

I am also ranking Burhan Azeem as my #1 choice. I agree with everything Josh says. And I've also personally been really impressed with Burhan's amazing combination of commitment to Cambridge, deep thoughtfulness about the issues it faces and pragmatism and inclusiveness in his approach to them.

I am also ranking Burhan Azeem as my #1 choice. I agree with everything Josh says. And I've also personally been really impressed with Burhan's amazing combination of commitment to Cambridge, deep thoughtfulness about the issues it faces and pragmatism and inclusiveness in his approach to them.

I'll shortly write a longer post, but I just wanted to say that I'm ranking Burhan Azeem as my #1 City Council choice, largely because of his relentless and successful push to fix our city's housing policy (largely by eliminating zoning restrictions that drive up rents and sales prices).

For the first time in a generation, triple-deckers and affordable apartments are legal again in Cambridge.

Impossible? It wasn’t.

Inevitable? It’s wasn’t that either.

It was a choice.

Vote Burhan #1 on Nov 4th and keep choosing housing.

Impossible? It wasn’t.

Inevitable? It’s wasn’t that either.

It was a choice.

Vote Burhan #1 on Nov 4th and keep choosing housing.

November 3, 2025 at 6:19 PM

I am also ranking Burhan Azeem as my #1 choice. I agree with everything Josh says. And I've also personally been really impressed with Burhan's amazing combination of commitment to Cambridge, deep thoughtfulness about the issues it faces and pragmatism and inclusiveness in his approach to them.

People post too many memes.

October 28, 2025 at 10:33 PM

People post too many memes.

Being an Anglo-Saxon country not great for borrowing costs right now.

October 27, 2025 at 7:15 PM

Being an Anglo-Saxon country not great for borrowing costs right now.

This graph may or may not say a lot about the world over the last decade.

October 27, 2025 at 12:58 PM

This graph may or may not say a lot about the world over the last decade.

CEO pay has stagnated for the last quarter century.

October 26, 2025 at 5:41 PM

CEO pay has stagnated for the last quarter century.

Fixed by John Cambpell & Tarun Ramadorai is an important book--drawing on up-to-date research, grounded in experience in the US, UK and India, argues persuasively for more consumer finance regulation--an issue that has almost entirely faded from the debate. www.goodreads.com/review/show/...

Jason Furman's review of Fixed

5/5: Fixed is a terrific book about how badly broken personal finance is—and what should be done about it. I particularly appreciated the unique (to my knowledge) way in which this book is deeply grou...

www.goodreads.com

October 26, 2025 at 3:06 PM

Fixed by John Cambpell & Tarun Ramadorai is an important book--drawing on up-to-date research, grounded in experience in the US, UK and India, argues persuasively for more consumer finance regulation--an issue that has almost entirely faded from the debate. www.goodreads.com/review/show/...

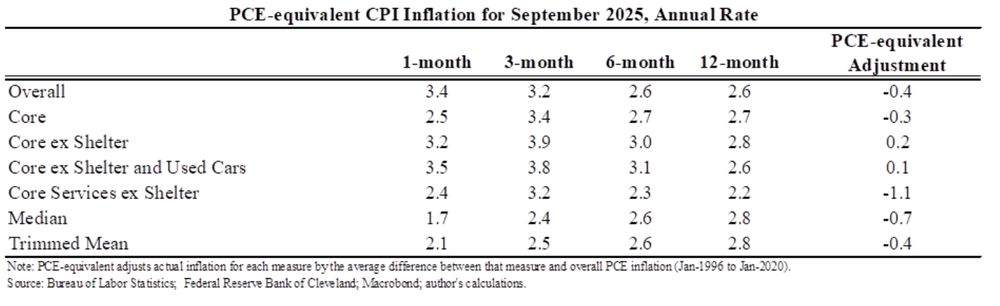

The CPI-based ecumenical underlying inflation measure was 2.7% in September, up 0.1pp from August (and the same as the PCE-based measure for August).

This is the median 7 concepts over 3, 6 and 12 months.

My own judgment is closer to 2.5%, maybe a tiny bit below.

This is the median 7 concepts over 3, 6 and 12 months.

My own judgment is closer to 2.5%, maybe a tiny bit below.

October 26, 2025 at 2:45 PM

The CPI-based ecumenical underlying inflation measure was 2.7% in September, up 0.1pp from August (and the same as the PCE-based measure for August).

This is the median 7 concepts over 3, 6 and 12 months.

My own judgment is closer to 2.5%, maybe a tiny bit below.

This is the median 7 concepts over 3, 6 and 12 months.

My own judgment is closer to 2.5%, maybe a tiny bit below.

The Federal minimum wage was established in 1938.

It was in effect for about 85 years.

It has now, for better or worse, been effectively abolished.

It was in effect for about 85 years.

It has now, for better or worse, been effectively abolished.

October 26, 2025 at 2:28 PM

The Federal minimum wage was established in 1938.

It was in effect for about 85 years.

It has now, for better or worse, been effectively abolished.

It was in effect for about 85 years.

It has now, for better or worse, been effectively abolished.

If you call a bubble early you're not prescient, you're wrong.

If you bought the stock market on the day Alan Greenspan announced "irrational exuberance" you would have made money no matter what day you ended up selling.

(Don't @ me about inflation adjustment.)

If you bought the stock market on the day Alan Greenspan announced "irrational exuberance" you would have made money no matter what day you ended up selling.

(Don't @ me about inflation adjustment.)

October 24, 2025 at 1:47 PM

If you call a bubble early you're not prescient, you're wrong.

If you bought the stock market on the day Alan Greenspan announced "irrational exuberance" you would have made money no matter what day you ended up selling.

(Don't @ me about inflation adjustment.)

If you bought the stock market on the day Alan Greenspan announced "irrational exuberance" you would have made money no matter what day you ended up selling.

(Don't @ me about inflation adjustment.)

The government made the reasonable decision to release CPI data because needed to calculate Social Security COLAs.

Quick summary, core CPI annual rate:

1 month: 2.8%

3 months: 3.6%

6 months: 3.0%

12 months: 3.0%

Quick summary, core CPI annual rate:

1 month: 2.8%

3 months: 3.6%

6 months: 3.0%

12 months: 3.0%

October 24, 2025 at 1:30 PM

The government made the reasonable decision to release CPI data because needed to calculate Social Security COLAs.

Quick summary, core CPI annual rate:

1 month: 2.8%

3 months: 3.6%

6 months: 3.0%

12 months: 3.0%

Quick summary, core CPI annual rate:

1 month: 2.8%

3 months: 3.6%

6 months: 3.0%

12 months: 3.0%

The stock market is not the economy, Part 387

Productivity growth is often lagged, Part 129

Productivity growth before and after the dot.com bust

Productivity growth is often lagged, Part 129

Productivity growth before and after the dot.com bust

dot.co

October 23, 2025 at 1:35 PM

The stock market is not the economy, Part 387

Productivity growth is often lagged, Part 129

Productivity growth before and after the dot.com bust

Productivity growth is often lagged, Part 129

Productivity growth before and after the dot.com bust

I discuss bubbles, the macroeconomy and more with Ross Douthat. www.nytimes.com/2025/10/23/o...

Opinion | We Can Survive an A.I. Bust

We’ve been here before.

www.nytimes.com

October 23, 2025 at 1:33 PM

I discuss bubbles, the macroeconomy and more with Ross Douthat. www.nytimes.com/2025/10/23/o...

CBO is as good as it gets. But the world is hard to predict.

October 23, 2025 at 12:15 AM

CBO is as good as it gets. But the world is hard to predict.

If you're not surprised & puzzled about Treasuries being <4% then you're either a seer, incurious or have better things to wonder about.

Large deficits (albeit smaller than expected), capital demand, Fed independence risk, persistent inflation, uncertainty, all go the other way.

Large deficits (albeit smaller than expected), capital demand, Fed independence risk, persistent inflation, uncertainty, all go the other way.

October 20, 2025 at 10:43 PM

If you're not surprised & puzzled about Treasuries being <4% then you're either a seer, incurious or have better things to wonder about.

Large deficits (albeit smaller than expected), capital demand, Fed independence risk, persistent inflation, uncertainty, all go the other way.

Large deficits (albeit smaller than expected), capital demand, Fed independence risk, persistent inflation, uncertainty, all go the other way.

Three months ago I was wondering why jobs were so strong while GDP was so weak.

Now with additional data and revisions I'm wondering the opposite.

As always would place more weight on data messiness than any structural explanation (e.g., productivity, frozen labor market, etc)

Now with additional data and revisions I'm wondering the opposite.

As always would place more weight on data messiness than any structural explanation (e.g., productivity, frozen labor market, etc)

October 13, 2025 at 2:46 PM

Three months ago I was wondering why jobs were so strong while GDP was so weak.

Now with additional data and revisions I'm wondering the opposite.

As always would place more weight on data messiness than any structural explanation (e.g., productivity, frozen labor market, etc)

Now with additional data and revisions I'm wondering the opposite.

As always would place more weight on data messiness than any structural explanation (e.g., productivity, frozen labor market, etc)

According to official government data the unemployment rate was unchanged while the economy added 60,000 jobs in September.

In Canada.

In Canada.

October 10, 2025 at 1:46 PM

According to official government data the unemployment rate was unchanged while the economy added 60,000 jobs in September.

In Canada.

In Canada.

The other day a student asked me about the prevalence of insider trading in prediction markets. I now have an answer.

October 10, 2025 at 11:19 AM

The other day a student asked me about the prevalence of insider trading in prediction markets. I now have an answer.

Core PCE inflation rising lately, running ~3% annual rate.

But core PCE inflation ex portfolio services slowing lately, running just above 2% (when remeaned to reflect it usually runs low).

Some of the reinflation we've seen is rising stock prices counting as higher inflation.

But core PCE inflation ex portfolio services slowing lately, running just above 2% (when remeaned to reflect it usually runs low).

Some of the reinflation we've seen is rising stock prices counting as higher inflation.

October 6, 2025 at 8:05 PM

Core PCE inflation rising lately, running ~3% annual rate.

But core PCE inflation ex portfolio services slowing lately, running just above 2% (when remeaned to reflect it usually runs low).

Some of the reinflation we've seen is rising stock prices counting as higher inflation.

But core PCE inflation ex portfolio services slowing lately, running just above 2% (when remeaned to reflect it usually runs low).

Some of the reinflation we've seen is rising stock prices counting as higher inflation.

In 2000 & 2016 the Dems won the Presidential popular vote but lost the electoral college.

Just chance the opposite hasn't happened. Eg 2004: Kerry came closer in the EC than the popular vote.

This is the pop vote vote margin Dems would have needed in past elections to win EC.

Just chance the opposite hasn't happened. Eg 2004: Kerry came closer in the EC than the popular vote.

This is the pop vote vote margin Dems would have needed in past elections to win EC.

October 5, 2025 at 4:05 PM

In 2000 & 2016 the Dems won the Presidential popular vote but lost the electoral college.

Just chance the opposite hasn't happened. Eg 2004: Kerry came closer in the EC than the popular vote.

This is the pop vote vote margin Dems would have needed in past elections to win EC.

Just chance the opposite hasn't happened. Eg 2004: Kerry came closer in the EC than the popular vote.

This is the pop vote vote margin Dems would have needed in past elections to win EC.

Do you prefer Option 1 or Option 2? And why?

October 5, 2025 at 3:43 PM

Do you prefer Option 1 or Option 2? And why?

"In one respect, Breakneck is a classic work of a hedgehog. Dan Wang knows one big thing: China is run by engineers, and the United States is run by lawyers. He then applies that idea to many topics..."

My review of the excellent Breakneck. www.goodreads.com/review/show/...

My review of the excellent Breakneck. www.goodreads.com/review/show/...

Jason Furman’s review of Breakneck: China's Quest to Engineer the Future

5/5: In one respect, Breakneck is a classic work of a hedgehog. Dan Wang knows one big thing: China is run by engineers, and the United States is run by lawyers. He then applies that idea to many topics,...

www.goodreads.com

October 4, 2025 at 12:13 PM

"In one respect, Breakneck is a classic work of a hedgehog. Dan Wang knows one big thing: China is run by engineers, and the United States is run by lawyers. He then applies that idea to many topics..."

My review of the excellent Breakneck. www.goodreads.com/review/show/...

My review of the excellent Breakneck. www.goodreads.com/review/show/...

The United States ended FY 2025 with $30.287 trillion of debt.

That is likely 99.9% of GDP, up from 98.2% last year.

Note CBO's January forecast was 99.9% of GDP.

In June CEA projected that if OBBBA passed it would fall to 96.2% of GDP this year.

That is likely 99.9% of GDP, up from 98.2% last year.

Note CBO's January forecast was 99.9% of GDP.

In June CEA projected that if OBBBA passed it would fall to 96.2% of GDP this year.

October 1, 2025 at 9:06 PM

The United States ended FY 2025 with $30.287 trillion of debt.

That is likely 99.9% of GDP, up from 98.2% last year.

Note CBO's January forecast was 99.9% of GDP.

In June CEA projected that if OBBBA passed it would fall to 96.2% of GDP this year.

That is likely 99.9% of GDP, up from 98.2% last year.

Note CBO's January forecast was 99.9% of GDP.

In June CEA projected that if OBBBA passed it would fall to 96.2% of GDP this year.