Greg Cordell

@gregorypcordell.bsky.social

Army veteran; AT thru-hiker; CFA charterholder; LFC fan; football finance analysis here and on Substack (no paywall; link below).

https://gregcordell.substack.com/

https://gregcordell.substack.com/

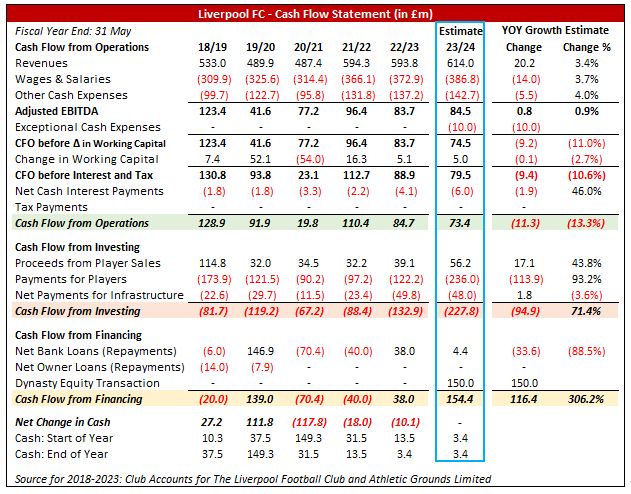

Updated cash flow stmt estimates are provided as well, but note that figures are highly speculative:

- Cash generated from operations est of ~ £74m

- Cash outflow for investment est of ~ £228m (net player: £180m; capex: £48m)

- Cash inflow from financing est of ~ £154m (assumed £150m from Dynasty).

- Cash generated from operations est of ~ £74m

- Cash outflow for investment est of ~ £228m (net player: £180m; capex: £48m)

- Cash inflow from financing est of ~ £154m (assumed £150m from Dynasty).

January 23, 2025 at 2:50 PM

Updated cash flow stmt estimates are provided as well, but note that figures are highly speculative:

- Cash generated from operations est of ~ £74m

- Cash outflow for investment est of ~ £228m (net player: £180m; capex: £48m)

- Cash inflow from financing est of ~ £154m (assumed £150m from Dynasty).

- Cash generated from operations est of ~ £74m

- Cash outflow for investment est of ~ £228m (net player: £180m; capex: £48m)

- Cash inflow from financing est of ~ £154m (assumed £150m from Dynasty).

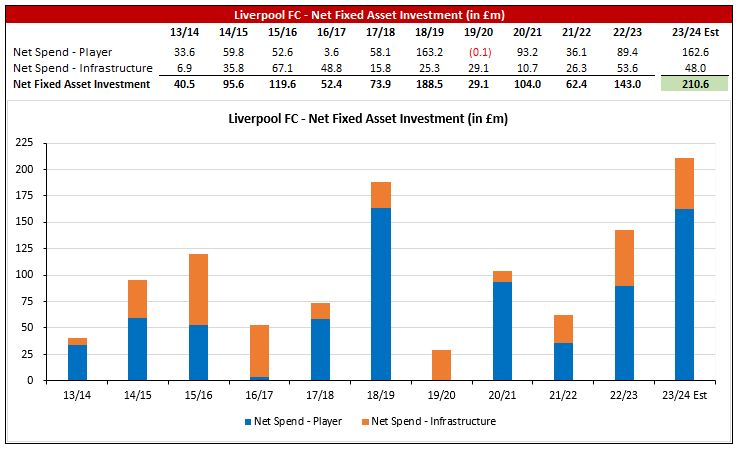

To supplement P&L estimates, a note that I've estimated net fixed asset spend (net player spend + net infrastructure spend) to be ~ £211m, which would reflect a new club high. In particular, I've estimated player net spend in accts to be ~ £163m (much higher than the ~ £95m on Transfermarkt).

January 23, 2025 at 2:50 PM

To supplement P&L estimates, a note that I've estimated net fixed asset spend (net player spend + net infrastructure spend) to be ~ £211m, which would reflect a new club high. In particular, I've estimated player net spend in accts to be ~ £163m (much higher than the ~ £95m on Transfermarkt).

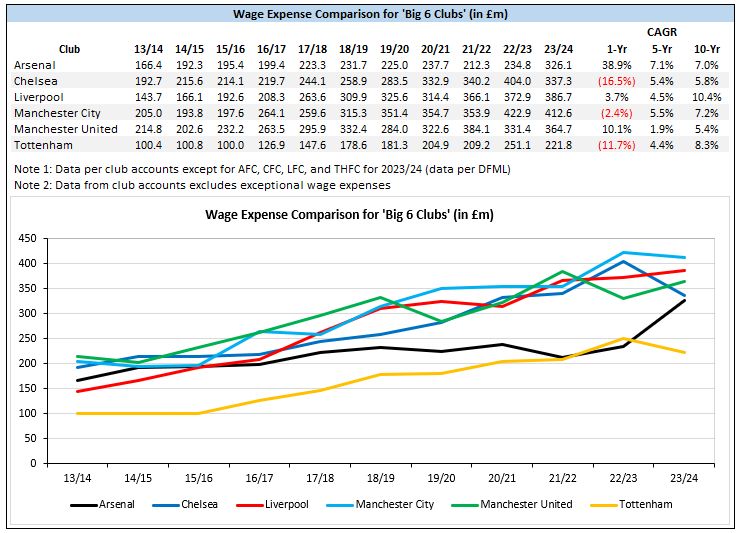

Each of CFC and THFC saw total wages decrease by double digits (note: not in UCL), while MUFC and AFC (return to UCL) each saw doubt digit increases. Interestingly, LFC's wages increased by ~ 4% YOY (general expectation was a step down).

As a cohort, wages in aggregate increased by ~ 2%.

As a cohort, wages in aggregate increased by ~ 2%.

January 23, 2025 at 2:42 PM

Each of CFC and THFC saw total wages decrease by double digits (note: not in UCL), while MUFC and AFC (return to UCL) each saw doubt digit increases. Interestingly, LFC's wages increased by ~ 4% YOY (general expectation was a step down).

As a cohort, wages in aggregate increased by ~ 2%.

As a cohort, wages in aggregate increased by ~ 2%.

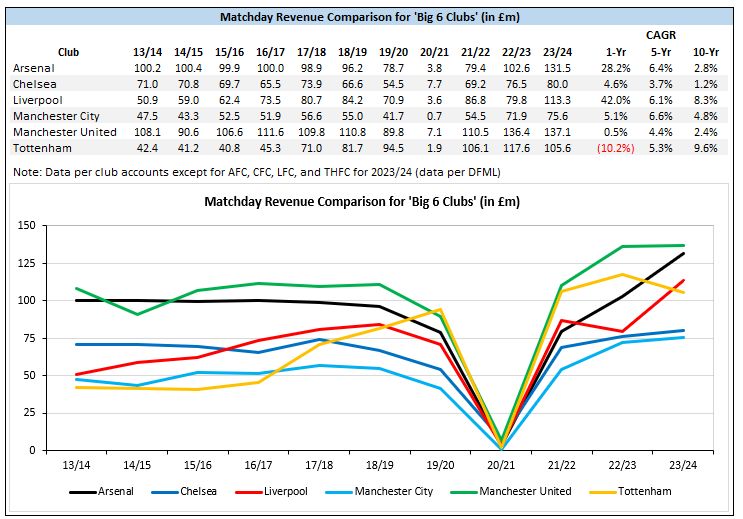

Liverpool and Arsenal each exhibited sizeable matchday revenue growth, w/ Liverpool exceeding £100m for the first time.

On an aggregate basis, matchday revenue increased by ~ 10% YOY across the cohort.

On an aggregate basis, matchday revenue increased by ~ 10% YOY across the cohort.

January 23, 2025 at 2:42 PM

Liverpool and Arsenal each exhibited sizeable matchday revenue growth, w/ Liverpool exceeding £100m for the first time.

On an aggregate basis, matchday revenue increased by ~ 10% YOY across the cohort.

On an aggregate basis, matchday revenue increased by ~ 10% YOY across the cohort.

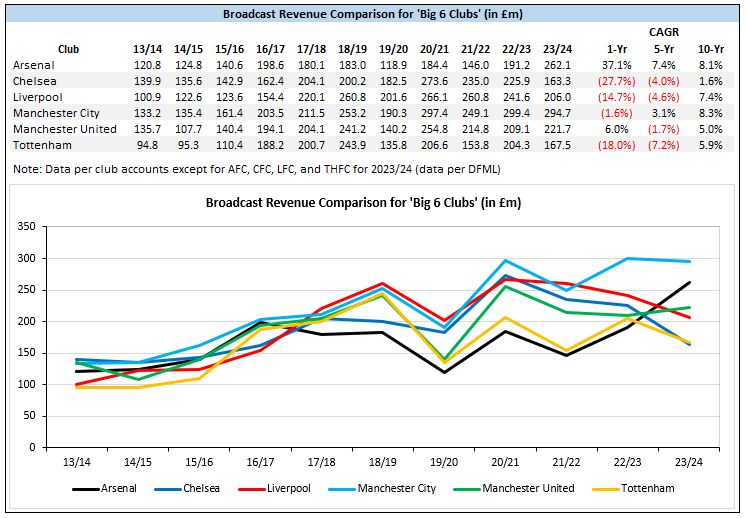

Three of six from the cohort experienced double digit YOY declines in broadcast revenue (due to missing out on UCL in 2023/24 after participating in 2022/23). In aggregate, broadcast revenue decreased ~ 4% YOY for Big 6 clubs. Arsenal again the club exhibiting standout growth within the group.

January 23, 2025 at 2:42 PM

Three of six from the cohort experienced double digit YOY declines in broadcast revenue (due to missing out on UCL in 2023/24 after participating in 2022/23). In aggregate, broadcast revenue decreased ~ 4% YOY for Big 6 clubs. Arsenal again the club exhibiting standout growth within the group.

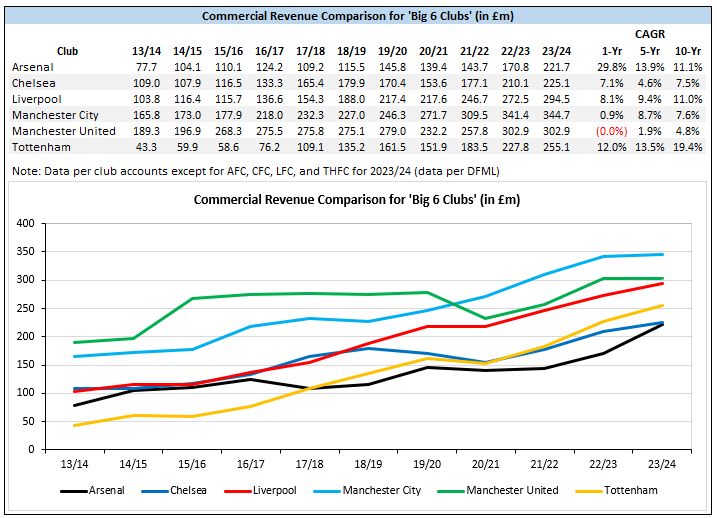

Commercial growth was generally flat for the Manchester clubs, but each other Big 6 club exhibited 7%+ YOY growth (AFC the standout at ~ 30%).

Note that LFC categorize comm differently vs Deloitte and might report comm rev ~ £10m to £15m in accts (w/ MD and broad lower) if similar to prior years.

Note that LFC categorize comm differently vs Deloitte and might report comm rev ~ £10m to £15m in accts (w/ MD and broad lower) if similar to prior years.

January 23, 2025 at 2:42 PM

Commercial growth was generally flat for the Manchester clubs, but each other Big 6 club exhibited 7%+ YOY growth (AFC the standout at ~ 30%).

Note that LFC categorize comm differently vs Deloitte and might report comm rev ~ £10m to £15m in accts (w/ MD and broad lower) if similar to prior years.

Note that LFC categorize comm differently vs Deloitte and might report comm rev ~ £10m to £15m in accts (w/ MD and broad lower) if similar to prior years.

Yes. I'll provide separate threads today w/ DFML summary data for PL clubs and 2023/24 LFC high level estimates.

January 23, 2025 at 2:28 PM

Yes. I'll provide separate threads today w/ DFML summary data for PL clubs and 2023/24 LFC high level estimates.

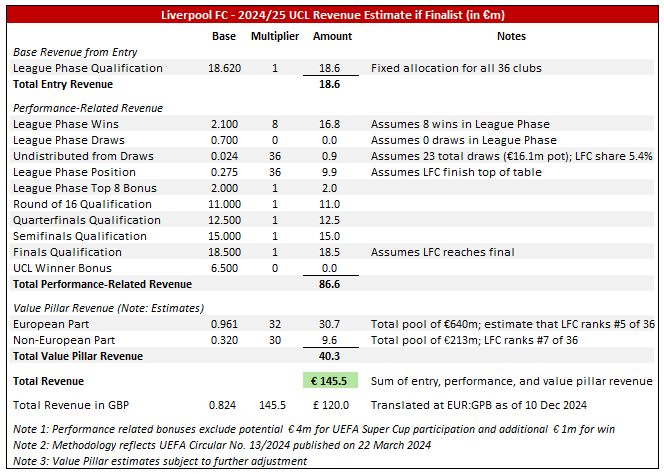

My est is ~ €145m if LFC win the final two league matches and advance to the final.

My interpretation of the 2024-2027 model is advancement of other PL clubs won't shift distributions in the same way as for 2021-2024. There is uncertainty on Euro Part Value Pillar, but I went slightly conservative.

My interpretation of the 2024-2027 model is advancement of other PL clubs won't shift distributions in the same way as for 2021-2024. There is uncertainty on Euro Part Value Pillar, but I went slightly conservative.

December 11, 2024 at 4:44 AM

My est is ~ €145m if LFC win the final two league matches and advance to the final.

My interpretation of the 2024-2027 model is advancement of other PL clubs won't shift distributions in the same way as for 2021-2024. There is uncertainty on Euro Part Value Pillar, but I went slightly conservative.

My interpretation of the 2024-2027 model is advancement of other PL clubs won't shift distributions in the same way as for 2021-2024. There is uncertainty on Euro Part Value Pillar, but I went slightly conservative.

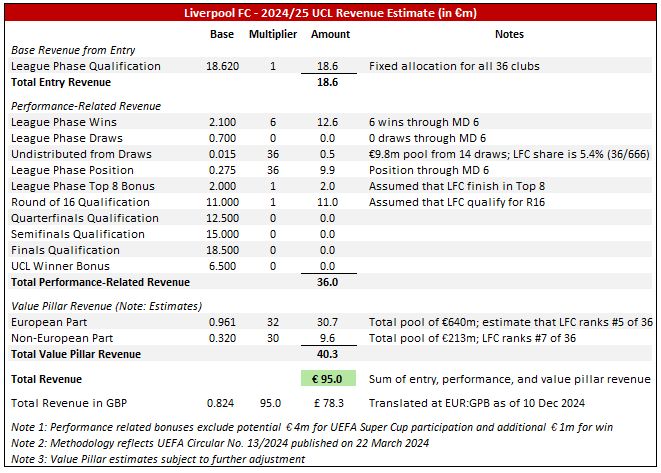

FWIW, attached is a figure with estimated 2024/25 UCL revenue to date based on UEFA's distribution circular. I have it at ~ €95m (~ £78m) w/ up to ~ €57m more in play based on performance.

December 11, 2024 at 2:22 AM

FWIW, attached is a figure with estimated 2024/25 UCL revenue to date based on UEFA's distribution circular. I have it at ~ €95m (~ £78m) w/ up to ~ €57m more in play based on performance.

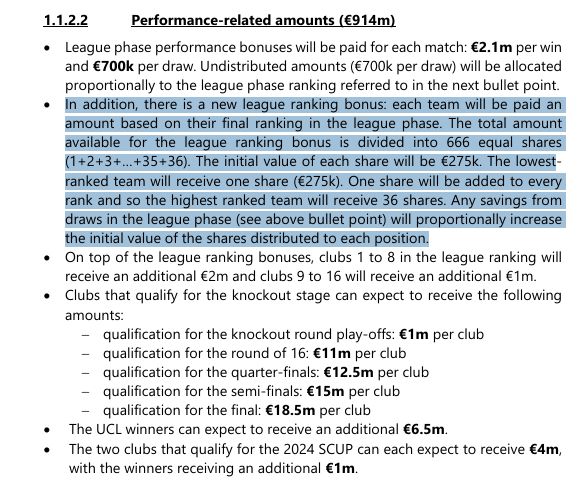

There is a distribution tranche for league phase position, w/ each position worth €275k. Therefore, finishing first ('36 shares') results in €9.9m in prize money that is additive to league phase per match and KO advancement bonuses.

December 11, 2024 at 12:46 AM

There is a distribution tranche for league phase position, w/ each position worth €275k. Therefore, finishing first ('36 shares') results in €9.9m in prize money that is additive to league phase per match and KO advancement bonuses.

Plus there is a benefit to finishing as a stronger seed as it relates to the KO draw process / bracket. A lot of folks seem to be under the impression that there is no differentiation between first and eighth.

December 9, 2024 at 11:31 PM

Plus there is a benefit to finishing as a stronger seed as it relates to the KO draw process / bracket. A lot of folks seem to be under the impression that there is no differentiation between first and eighth.